Not all financial obligations appear on the balance sheet. One commonly overlooked issue is contingent liability, potential obligations arising from future events, such as unresolved lawsuits, product warranties, or pending tax assessments.

As businesses seek better control over these hidden risks, Singapore’s accounting software market is projected to grow at a compound annual growth rate (CAGR) of 4.2% from 2025 to 2031, driven by tools that automate tracking and improve compliance with financial regulations.

To address this, HashMicro Accounting offers an intelligent system that automates the identification, recording, and monitoring of contingent liabilities, helping businesses mitigate risks and make more informed financial decisions.

Let’s explore how the right accounting solution can transform the way your business manages these hidden financial risks.

Table of Content:

Table of Content

Key Takeaways

|

What Is Contingent Liability?

Contingent liability is a potential financial obligation that may occur depending on the outcome of a future event. It becomes an actual liability only if certain conditions are met, such as losing a lawsuit or triggering a product warranty.

These liabilities are not guaranteed to happen, but they must be evaluated and disclosed if the likelihood of occurrence is probable and the amount can be reasonably estimated. Common examples include pending legal cases, government investigations, and environmental cleanup responsibilities.

Failing to recognize or disclose contingent liabilities properly can mislead stakeholders and distort a company’s financial health. This is why businesses need a structured approach, backed by technology, to track these uncertainties before they become real costs.

3 Types of Contingent Liability

Contingent liabilities come in several forms, each with its own potential risk and accounting treatment. Here are the three most common types:

1. Probable contingent liabilities

These are liabilities that are likely to occur and can be reasonably estimated. According to accounting standards, they must be recorded in the financial statements.

Examples include pending lawsuits with strong evidence against the company or obligations under guarantees that are likely to be claimed.

2. Possible contingent liabilities

These liabilities might occur, but the outcome is uncertain and cannot be easily predicted. While they are not recorded in the financial statements, they must be disclosed in the notes. An example would be a legal dispute where the outcome is unclear and could go either way.

3. Remote contingent liabilities

These are liabilities with very low chances of occurring. Because the likelihood is minimal and they usually can’t be estimated, they are neither recorded nor disclosed unless the impact could be significant. An example might be a lawsuit with no legal basis or a highly unlikely government penalty.

Understanding these types helps businesses prioritize risk assessment and determine which liabilities need closer monitoring and reporting.

How Contingent Liabilities Work

Contingent liabilities function based on uncertainty—they only become actual liabilities if a specific future event occurs. The accounting treatment depends on two key factors: the probability of the event happening and whether the potential amount can be estimated.

If both are true and the event is likely, the liability must be recorded in the financial statements. If the outcome is uncertain but possible, it should be disclosed in the notes to the financial report. If the chance is remote, it may not require any action unless it’s material.

For example, if a company is sued and legal counsel believes it will likely lose and the damages can be estimated, the amount should be reported as a liability. But if the case is weak or the outcome can’t be predicted, it’s noted only for transparency.

This system ensures stakeholders receive a fair view of a company’s financial exposure, even when the risks are not yet realized.

Example of a Contingent Liability

A construction firm signs a performance bond as part of a government infrastructure contract. The bond guarantees that the project will be completed on time and within the agreed specifications. If the firm fails to meet the terms, a third-party surety provider will compensate the government, and the firm will be obligated to reimburse that provider.

Partway through the project, the company encounters unexpected material shortages and labor strikes, raising the risk of delay. Based on internal assessments, there is a high probability of missing the deadline, with an estimated financial exposure of around SGD 700,000.

Because the potential obligation is likely and the amount can be reasonably estimated, this situation qualifies as a contingent liability that must be recognized in the financial statements.

On the other hand, if the likelihood of default were low, the obligation would only need to be disclosed in the notes, or not at all if the risk is minimal.

This example illustrates how contingent liabilities don’t only come from lawsuits or legal claims—they can also arise from contractual guarantees and operational risks, especially in project-based industries.

How Businesses Manage Contingency Liabilities

Effectively managing contingent liabilities is crucial for maintaining financial stability and fostering trust among stakeholders.

Businesses typically follow a structured approach that involves identification and assessment. Managing contingent liabilities requires a proactive and structured approach to reduce risk and maintain financial integrity. Here are the key steps businesses typically follow:

1. Identifying potential liabilities

Companies begin by reviewing operations, contracts, and legal matters to identify situations that could lead to future financial obligations, such as pending litigation, loan guarantees, or environmental issues.

2. Assessing likelihood and impact

Each potential liability is assessed based on its probability (probable, possible, or remote) and whether the financial impact can be estimated. This evaluation determines how the liability should be treated in financial reporting.

3. Recording or disclosing

If the liability is both likely and measurable, it is recorded directly in the financial statements. If possible, it’s disclosed in the notes. If the risk is remote, no action is typically required—unless the potential impact is material.

4. Ongoing monitoring

Conditions can change. Legal outcomes, negotiations, or shifts in business operations may alter the status of a liability. Regular reviews ensure that any changes are promptly reflected in reports.

5. Implementing internal controls and systems

To support accurate tracking and reporting, businesses often utilize integrated systems that enable real-time monitoring, standardized documentation, and compliance with financial reporting standards such as IFRS or GAAP.

By actively managing contingent liabilities, businesses can avoid unexpected financial shocks and present a clearer, more trustworthy picture of their financial position to stakeholders.

How HashMicro ERP Can Help Businesses Manage Contingent Liabilities

Managing contingent liability requires accuracy, consistency, and visibility, which are the qualities that manual processes often lack. HashMicro’s accounting system addresses these challenges with an integrated platform that simplifies how businesses identify, monitor, and respond to potential financial obligations.

The system provides real-time tracking of liability-related entries, allowing finance teams to stay updated on the status of potential risks. You can explore these capabilities through a free demo, providing a hands-on look at how the system streamlines liability management.

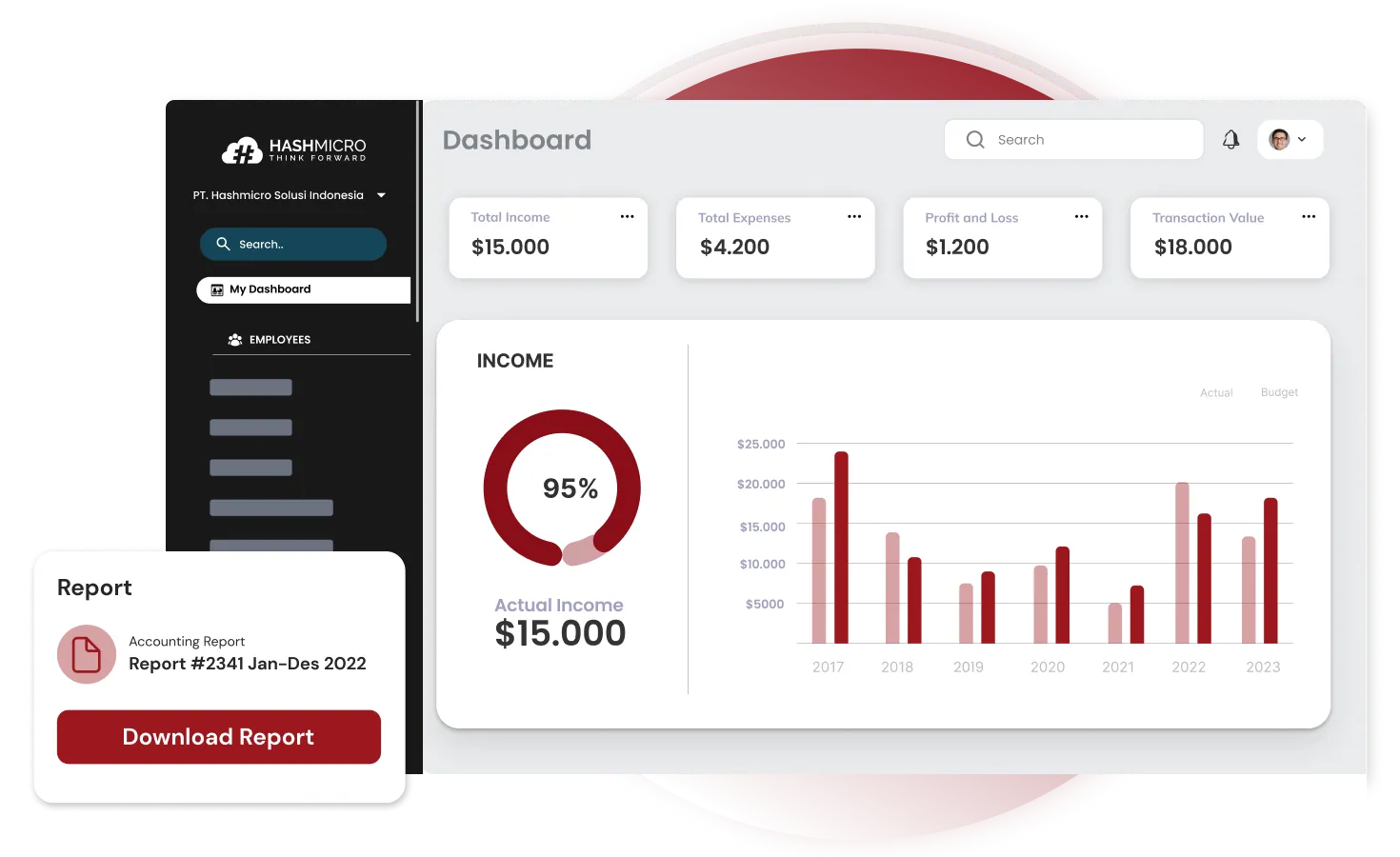

Key features of HashMicro Accounting System:

- Cash Flow Reports: Provide detailed insights into incoming and outgoing cash, supporting better liquidity management and financial planning.

- Forecast Budget: Assists in budgeting by using historical data and financial projections to allocate resources more efficiently.

- Budget S Curve: Provides a visual representation of budget progression through an S-curve, enabling the tracking of spending trends against planned allocations.

- Financial Statement with Budget Comparison: Displays actual financial results alongside budgeted figures, making it easier to spot variances and evaluate performance.

- Automated Currency Update: Automatically refreshes exchange rates from reliable sources to ensure accurate calculations in international transactions.

- Risk Assessment Log: Tracks and records potential financial risks, including contingent liabilities, allowing businesses to monitor unresolved issues and assess their potential impact on cash flow and reporting.

Conclusions

Contingent liability is potential financial obligations that depend on the outcome of uncertain events, such as legal disputes, environmental issues, or contractual guarantees.

These liabilities are not immediate but can become actual financial burdens if certain conditions are met. Businesses must recognize and monitor contingent liabilities to prevent unexpected financial impacts that could disrupt cash flow and overall stability.

HashMicro Accounting offers a smart and efficient way to manage contingent liabilities. With features such as real-time tracking, automated alerts, centralized documentation, and AI-generated financial reports, the system enables businesses to maintain visibility over potential risks and stay financially prepared.

If you’re looking to strengthen your financial management and gain better control over contingent liabilities, try a free demo of HashMicro Accounting today and see how it can help you make more confident, data-driven decisions.

FAQ About Contingent Liability

-

What is a contingent asset with example?

Contingent assets are potential assets whose value relies on the outcome of external or non-operating factors. For instance, farmland may be considered a contingent asset, as its value is tied to the success of the crops grown and sold. A productive harvest boosts its worth, while a poor yield can reduce it.

-

What are contingent liabilities under IFRS?

It refers to either a potential obligation that hinges on the outcome of an uncertain future event, or an existing obligation where payment is unlikely or the amount cannot be reliably estimated.

-

How to recognize contingent liabilities?

A contingent liability should be recorded when it is likely that a loss has occurred and the amount can be estimated with reasonable accuracy.