In today’s fast-paced business environment, sticking to manual accounting is no longer an option. Cloud accounting software has become a game-changer for Singapore businesses by centralizing invoicing, payroll, and tax reporting in one secure platform.

However, choosing the right accounting tool can feel overwhelming with so many options available. The best accounting software should align with your business needs, offering features that truly add value. That’s why we’ve compiled a list of some of the best accounting software solutions to help you make an informed decision.

As an award-winning ERP provider, HashMicro goes beyond the basics with a comprehensive accounting software that automates repetitive tasks, minimizes human error, and provides insights to support smarter decision-making. Experience it firsthand by accessing our free demo

Key Takeaways

|

Shortlisted Best Cloud Accounting Software

Based on my review of available solutions, I have identified several cloud accounting software that stand out for businesses in Singapore. With capabilities such as automated bookkeeping, secure data storage, and real-time financial insights, these platforms can help companies enhance efficiency and ensure compliance in 2025.

Best Because

Intuitive interface and powerful tools that simplify bookkeeping and financial management

Best Because

User-friendly automation that connects businesses with banks, advisors, and real-time numbers

Best Because

Robust cloud-based platform that separates accounting and payroll for focused management

Best Because

Simple and intuitive platform that streamlines essential financial management tasks

Best Because

Scalable ERP solution with integrated financial and business management tools

Best Because

Seamless integrations and automation that enhance financial management efficiency

What is Cloud Accounting Software?

Accounting software is a must-have for businesses as it plays a crucial role in maintaining accurate records, ensuring compliance, and enabling smarter financial decisions. Here’s how it benefits businesses:

- Keeps finances accurate: It records income, expenses, and payments correctly, ensuring compliance with ACRA regulations and making financial reporting stress-free.

- All-in-one financial tools: It handles invoices, bills, bank reconciliation, and reports—everything needed to meet Singapore’s financial standards.

- Smart automation: It simplifies GST billing, tracks cash flow, manages budgets, and calculates taxes, making IRAS compliance easier.

- Fits all business sizes: Whether small or large, it offers features and pricing that match different needs in Singapore’s business landscape.

- Reliable financial reports: It generates key reports like income statements and balance sheets, helping businesses stay tax-ready and make better financial decisions.

Managing finances doesn’t have to be a headache. The right software takes the stress out of numbers, handling the heavy lifting, so you can focus on growing your business instead of drowning in spreadsheets.

21 Best Cloud Accounting Software Singapore for 2025

Choosing the right accounting software can be hard when there are numerous providers, and that’s why it is crucial for you to choose the best one.

With that in mind, we have curated the 21 best accounting software options for you to choose from and find the best solution that fits your business needs. Let’s start with the first one:

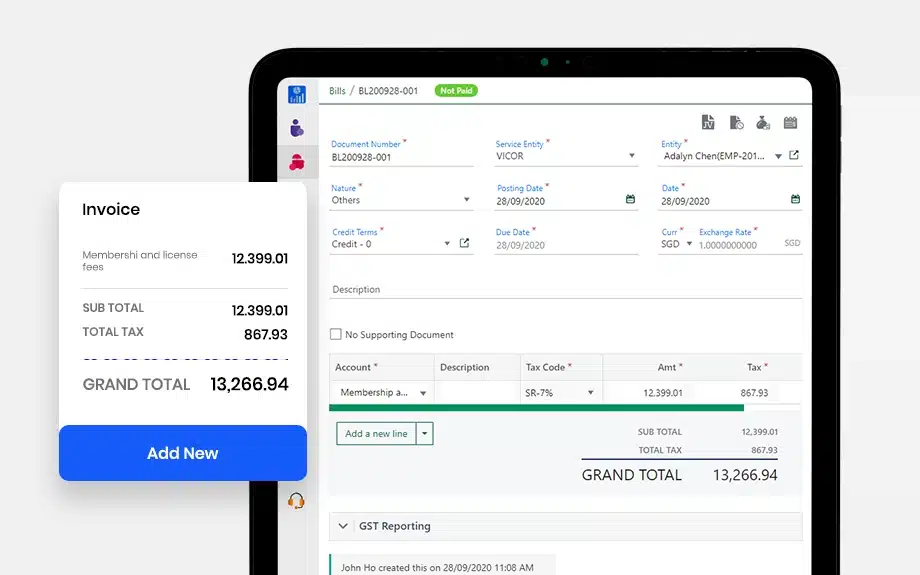

1. HashMicro Accounting Software

HashMicro’s Accounting Software is a comprehensive tool for automating financial management tasks. Trusted by over 2,000 leading Southeast Asian enterprises, it seamlessly integrates digital financial management, inventory management, CRM, and purchasing into a single platform.

Moreover, HashMicro’s Accounting Software is a cloud-based accounting software designed for flexibility and scalability. With automated processes, secure storage, and seamless integration with other business functions, this cloud accounting software helps companies streamline financial operations and make data-driven decisions effortlessly.

To fully understand how the best accounting system software can optimize financial management, HashMicro offers a free product tour and consultation. This hands-on experience allows potential users to see the software’s features firsthand.

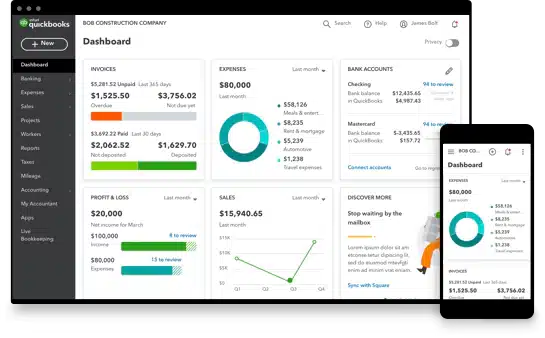

2. Accounting System Software QuickBooks

QuickBooks is one of the best cloud accounting software in Singapore, and it was developed by Intuit. It provides a system that is either desktop-based or cloud-based online. The features offered include managing inventory, managing cash, and so on.

One of their main features is a feature that categorizes each accounting activity so that users can easily search for transactions.

Why we choose this software:

We chose QuickBooks Intuit for its intuitive interface and powerful accounting tools that make financial management and bookkeeping easy for businesses of all sizes.

Features:

- Invoicing

- Expense tracking

- Payroll management

- Reporting

| Pros | Cons |

|

|

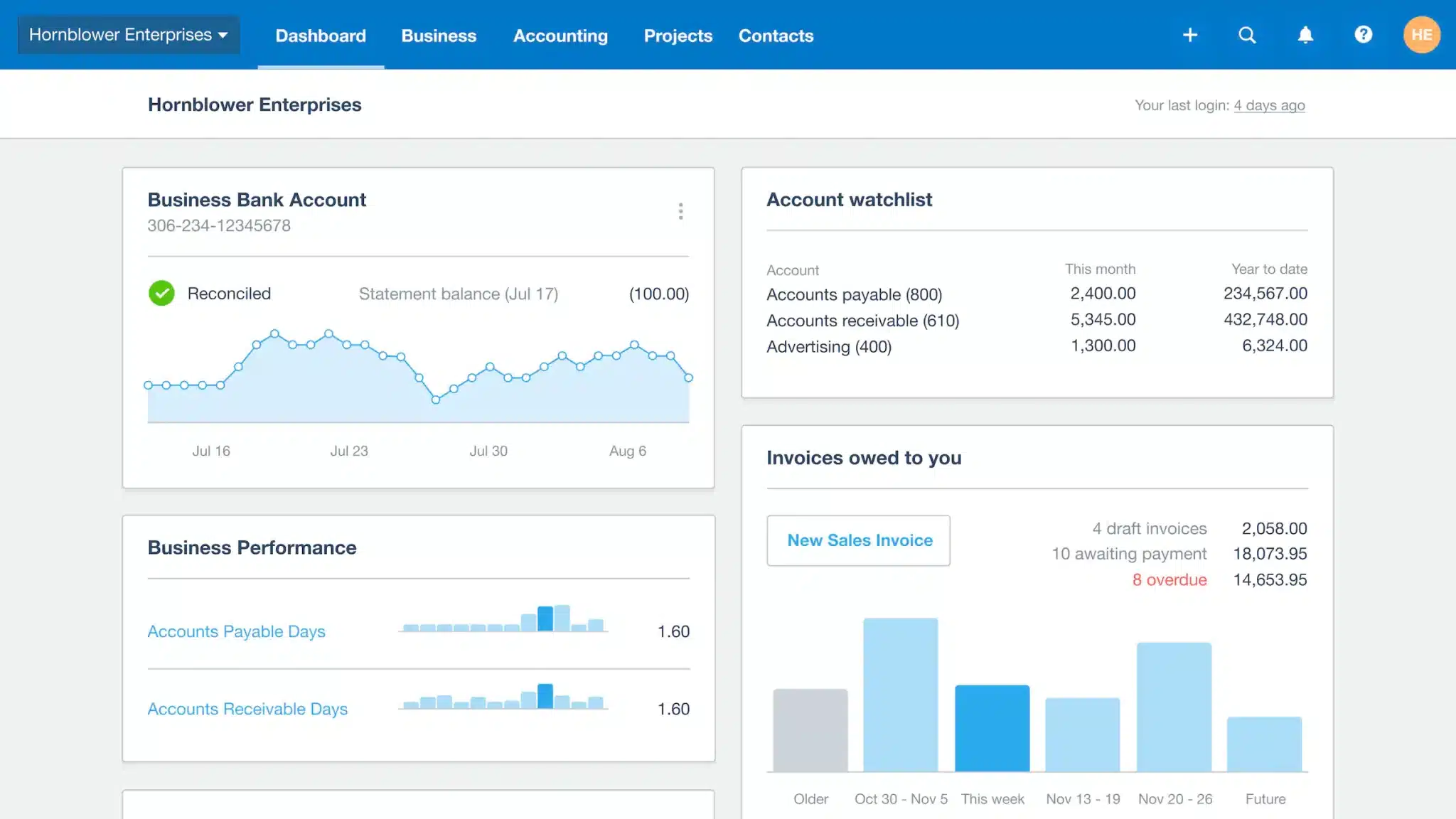

3. Finance Software Xero

Xero software is one of the popular accounting apps in Singapore that can automate accounting processes within your company. This accounting system software can connect business owners with their numbers, banks, and advisors anytime.

Features owned by Xero range from paying bills, claiming expenses, bank connections, managing contacts, and tracking projects. Xero has various features that third parties can use.

Why choose this software:

We chose Xero Accounting Software for its user-friendly features that simplify financial management and streamline bookkeeping processes for businesses of all sizes.

Features:

- Bank reconciliation

- Online invoicing

- Expense claims

- Payroll

| Pros | Cons |

|

|

Find more best accounting software in Singapore that is as good as Xero by checking out our other articles about Xero software.

4. Cloud Accounting Software Sage Cloud

The journey of establishing Sage software began in 1981. To date, more than 21 countries have become customers. Sage provides accounting system software for businesses in Singapore.

Unlike other online best accounting software Singapore providers, Sage provides two different features between the accounting process and employee payroll to be more focused. In addition, the Sage interface is also user-friendly, so it is suitable for businesses.

Why we chose this accounting software:

We chose Sage Cloud for its robust features and cloud-based accessibility, enabling seamless financial management and real-time business collaboration.

Features:

- Stock and inventory management

- Project tracking

- Bank integration

- Online invoicing

| Pros | Cons |

|

|

5. Wave Accounting System Software

Wave is an accounting software company in Singapore that provides financial management solutions. It offers a range of features, including invoicing, accounting, payroll, and receipt scanning, all accessible from a user-friendly dashboard.

Why we chose this accounting software:

We chose Wave for its user-friendly platform that offers comprehensive financial management tools, perfect for businesses with simpler needs.

Features:

- Personal Finance

- Expense tracking

- Receipt scanning

| Pros | Cons |

|

|

6. Financial Software SAP Business One

SAP Business One is a Singapore accounting software company designed for enterprise business. It offers comprehensive features to help businesses manage their financial operations, including invoicing, accounting, expense management, and payroll processing.

SAP also offers a range of integrations with other software applications, such as payment and e-commerce platforms, making it easy for businesses to connect with other tools.

Why we chose this accounting software:

We chose SAP Business One for its integrated, scalable ERP solutions that provide comprehensive business management capabilities, which are ideal for growing enterprises.

Features:

- Financial Accounting

- Inventory management

- CRM integration

- Multi-location support

| Pros | Cons |

|

|

7. Cloud Accounting Software Oracle NetSuite

Oracle NetSuite is an accounting system software that offers a range of features to help businesses manage their finances. These include bank feeds automatically importing transactions from bank accounts, credit cards, and PayPal accounts.

This Singapore cloud accounting software also provides tools for managing sales, purchasing, and inventory and allows businesses to generate professional-looking invoices and quotes.

Why we chose this accounting software:

We chose Oracle NetSuite for its robust cloud-based ERP solutions that offer extensive financial management and operational efficiency for businesses of all sizes.

Features:

- E-commerce integration

- Scalability

- CRM integration

- Financial management

| Pros | Cons |

|

|

8. FreshBooks Accounting Software Singapore

FreshBooks is a business accounting software in Singapore that provides invoicing, accounting, expense management, and time-tracking features. With its user-friendly interface and comprehensive features, businesses can easily manage their financial operations, generate professional-looking invoices and estimates, track expenses and time, and reconcile bank accounts.

Why we chose this accounting software:

We chose FreshBooks for its easy-to-use invoicing and accounting features, which streamline financial management and enhance productivity.

Features:

- Time tracking

- Client Portal

- Project management

- Invoicing

| Pros | Cons |

|

|

9. Zoho Books

Zoho Books is one of the best accounting software in Singapore, and it is designed for businesses. The software provides capabilities for tracking billable hours, generating professional-looking invoices, reconciling bank accounts, managing inventory, and generating financial reports.

Why we chose this accounting software:

We chose Zoho Books for its accounting features and seamless integration capabilities. These provide businesses with efficient financial management and enhanced workflow automation.

Features:

- Inventory management

- Bank reconciliation

- Collaboration

- Expense tracking

| Pros | Cons |

|

|

10. Trulysmall Singapore Software

Trulysmall is an open-source accounting system software solution designed for businesses. Its features include accounting, invoicing, inventory management, and point-of-sale capabilities.

With Trulysmall, businesses can easily manage their financial operations, generate professional-looking invoices, keep track of inventory levels, manage customer and supplier accounts, and reconcile bank accounts.

Why we chose this accounting software:

We chose TrulySmall for its simple and efficient accounting tools, making financial management straightforward and hassle-free.

Features:

- Digital payments

- Automatic posting

- Multi-currency

- Invoicing

| Pros | Cons |

|

|

11. KashFlow Software

KashFlow is a cloud-based and one of the best accounting software in Singapore designed specifically for UK businesses. It is tailored to comply with UK tax laws and integrates seamlessly with HMRC, making it ideal for handling VAT, payroll, and other tax-related matters.

Why we chose this accounting software:

We chose KashFlow for its intuitive, cloud-based accounting software that simplifies financial management and streamlines business bookkeeping.

Features:

- Online invoicing

- Reporting

- Payroll

- All-in-one account

| Pros | Cons |

|

|

12. MYOB Software

MYOB Accounting is a comprehensive Singapore accounting software with various features and functionalities. This software is known for its ease of use and efficient handling of accounting tasks.

Why we chose this accounting software:

We chose MYOB Accounting for its powerful, user-friendly features that simplify financial management and support compliance.

Features:

- Cashflow management

- Bank integration

- Track income and expense

| Pros | Cons |

|

|

13. Lightspeed Software

Lightspeed is one of the best accounting software in Singapore, and it is designed for retail and restaurant businesses. Its features include point-of-sale (POS) capabilities, inventory management, customer relationship management, and e-commerce integration.

Why we chose this accounting software:

We chose Lightspeed for its integrated POS and accounting solutions, which enhance business operations and streamline financial management for the retail and hospitality industries.

Features:

- Billing management

- Cash management

- Online payments

| Pros | Cons |

|

|

14. Aspire Software

Aspire offers an all-in-one financial platform tailored for growing businesses. It features integrated solutions for expense management, global payments, and financial reporting. Its user-friendly interface provides seamless integration with major Singapore accounting software.

Why we chose this accounting software:

We chose Aspire for its innovative digital banking solutions, which simplify financial management and provide seamless integration with business accounting software in Singapore.

Features:

- Multiple currencies

- Remote access

- Online transaction

| Pros | Cons |

|

|

15. ZipBooks Software

ZipBooks is an accounting software in Singapore that simplifies financial management for businesses. It offers features such as simple bookkeeping, automated expense tracking, and intelligent reporting. However, some users may find its features too basic for complex accounting needs.

Why we chose this accounting software:

We chose ZipBooks for its smart, user-friendly Singapore accounting software that offers automated bookkeeping and detailed financial insights.

Features:

- Invoicing and billing

- Time tracking

- Mobile accounting

| Pros | Cons |

|

|

16. Financio Software

Financio is a comprehensive cloud accounting system software for Singapore businesses. It simplifies accounting tasks with features like automated bookkeeping, e-invoicing, and multi-user collaboration. It is designed for ease of use and offers a multilingual interface and responsive support.

Why we chose this accounting software:

We chose Financio for its straightforward, cloud-based accounting software that simplifies financial management.

Features:

- Billing and invoicing

- Reporting and analytics

- Multi-branch connectivity

| Pros | Cons |

|

|

17. SmartCursors Software

SmartCursors offers cloud accounting software in Singapore that is designed to provide businesses with comprehensive financial management. The platform includes automated bookkeeping, real-time financial reporting, and budget management, which help streamline accounting processes.

Why we chose this accounting software:

We chose SmartCursors for its innovative accounting solutions, which offer seamless integration, real-time financial tracking, and automation, making them ideal for modern businesses.

Features:

- Multiple entities

- Customer and vendor management

- Cash flow management

| Pros | Cons |

|

|

18. Highnix Software

Highnix offers a robust ERP system with integrated accounting software Singapore features. It supports multi-currency transactions and complies with stringent regulatory standards, including Singapore’s IRAS e-tax guidelines.

Why we chose this accounting software:

We chose Highnix for its advanced, user-friendly software in Singapore. This software provides comprehensive financial management and robust reporting tools tailored to businesses of all sizes.

Features:

- Integration with third-party applications

- Billing and invoicing

- Authentication and data backup

| Pros | Cons |

|

|

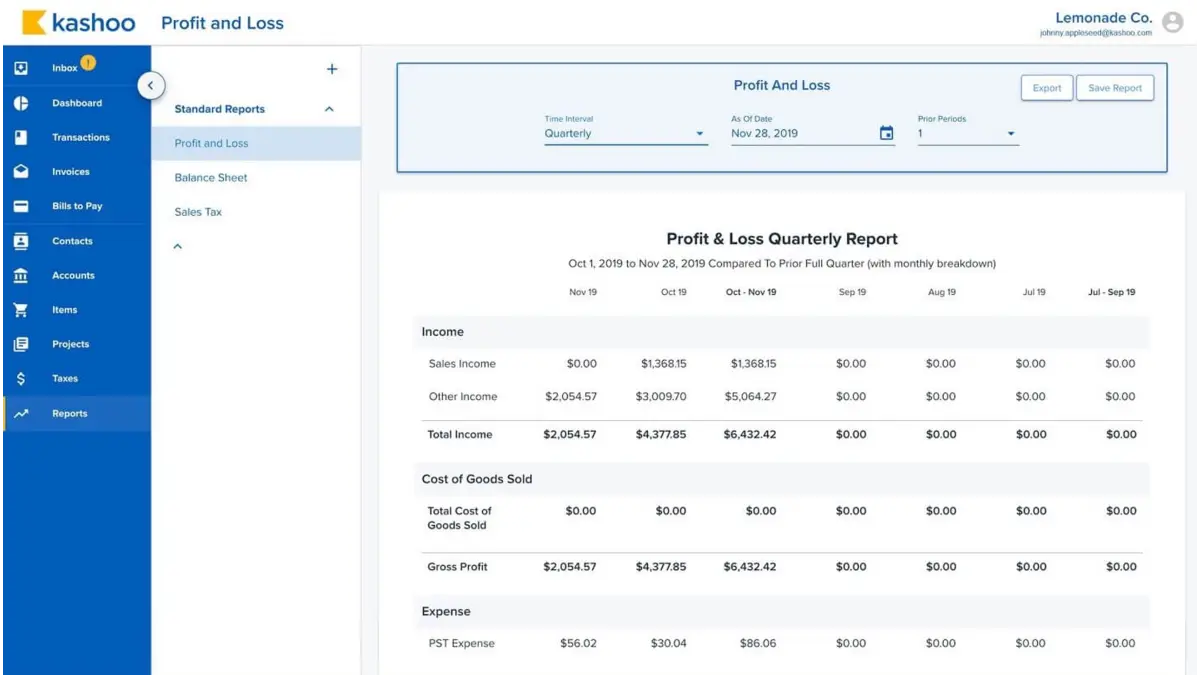

19. Kashoo Software

Kashoo is a cloud-based accounting software that aims to simplify financial management for small businesses. Its user-friendly interface and essential features allow business owners to access their financial data from any location, which can be beneficial for those who prioritize mobility.

Why we chose this accounting software:

Kashoo may be a suitable option for small businesses seeking a straightforward, cloud-based accounting solution, particularly for those who value simplicity and mobility.

Features:

- Invoicing: Enables users to create, send, and manage invoices with minimal effort.

- Expense Tracking: Provides real-time tracking of business expenses.

- Bank Reconciliation: Automates transaction syncing for accurate reconciliation.

| Pros | Cons |

|

|

20. AccountEdge Pro Software

This particular software being designed for small to medium-sized businesses, which caters to Mac users. It offers a range of features, including invoicing, payroll, and reporting, making it an option for those who prefer an offline accounting solution.

Why we chose this accounting software:

AccountEdge may be a suitable option for businesses with high mobility.

Features:

- Multi-User Access: Allows multiple users to work on a single company file simultaneously.

- Invoicing and Billing: Streamlines billing processes with efficient management of invoices and sales orders.

- Integrated Payroll Management: Includes features to simplify employee payment processes.

| Pros | Cons |

|

|

21. Akaunting Software

Akaunting is cloud-based, open-source software that simplifies small businesses’ financial management. It offers invoicing, expense tracking, and reporting. Focusing on usability and flexibility, Akaunting has gained global recognition and continues to innovate for modern business needs.

Why we chose this accounting software:

Cloud-based accessibility and continuous community-driven improvements ensure scalability and adaptability to business needs.

Features:

- Easy Invoicing: This feature streamlines the creation of professional invoices practically and can be customized according to your company’s needs or desires.

- Expense Tracking: Akaunting can manage and categorize all company expenses to properly manage your company’s financials.

- Financial Reporting: Akaunting can create detailed financial reports, including recording income, expenses, and cash flow, so the report is accurate for the company.

| Pros | Cons |

|

|

How to Choose the Ideal Accounting Software for Your Business

Selecting the ideal Singapore accounting software for your business can significantly impact your financial management and operational efficiency. To make the right choice, follow these key steps:

- Match Your Business Needs: Start by assessing your business size, transaction complexity, and industry requirements. This helps you focus on software options that align closely with your operational goals.

- Select the Right Feature: Look for essential features like invoicing, financial reporting, and tax management. Consider advanced tools such as automation and integration with other systems if they suit your workflow.

- Cloud vs. On-Premise: Cloud-based software offers remote access, easier maintenance, and lower upfront costs. On-premise solutions provide more control but require more IT resources and regular updates.

- Free vs. Paid Options: Free versions are suitable for basic needs but often lack scalability and support. Paid software provides broader functionality, stronger security, and dedicated customer service.

- Ease of Use: Choose a platform with an intuitive interface to minimize the learning curve and reduce user errors, especially if your team has limited technical expertise.

- Scalability: Make sure the software can grow with your business, whether by adding users, features, or integrating with more complex systems in the future.

- Support & Vendor Reputation: Opt for a provider known for responsive customer support and positive user reviews. Good training resources and documentation also help ensure smooth long-term use.

Choosing the right tool enhances financial management and efficiency. With this being said, consider your needs, features, scalability, and support before deciding on your choice.

Conclusion

Bookkeeping or accounting software in Singapore has become essential for companies because this crucial function cannot be performed poorly. When choosing the software for your accounting activities, you must select one that suits your company’s needs.

HashMicro Accounting Software is the best all-in-one system that integrates accounting, purchasing, and sales CRM. It streamlines financial processes and enhances efficiency. Manage your business seamlessly with automated, connected workflows.

So, what are you waiting for? Learn more by clicking the image below or schedule a HashMicro’s free demo now to experience the transformational power it brings to your business operations.

Frequently Asked Questions About Accounting Software

-

What is ERP accounting software?

ERP (Enterprise Resource Planning) accounting software is a business management solution that integrates various functions into a unified system. ERP accounting software provides a holistic approach by combining financial management with other essential business processes.

-

Which accounting software is the simplest to operate?

HashMicro Accounting Software is one of the easiest-to-use, feature-rich systems. It can be customized to customer needs and integrated with inventory management software, CRM, and purchasing systems to provide accurate data.

-

What is the difference between accounting software and ERP?

While accounting software and ERP systems are designed to improve business operations, they serve different purposes and offer distinct features. Understanding these differences can help businesses choose the right solution for their needs.

-

What are the types of accounting software in Singapore?

The types of accounting software available can be broadly categorized into the following: ERP software with accounting modules, cloud-based accounting software, and payroll and HR-integrated accounting software.

-

Should a small business get accounting software?

Yes, small businesses should consider investing in accounting software. Managing finances manually or with basic spreadsheets can be time-consuming and error-prone. Accounting software automates tasks such as recording transactions, managing invoices, and tracking expenses, saving time and reducing errors.

-

Why Are Security Features Important for Accounting Software in Singapore?

Security features are crucial for Singaporean businesses using accounting software, helping protect financial data with encryption and secure access controls. Compliance with the PDPA and added safeguards, such as real-time monitoring and backups.

-

How Do Industry-Specific Accounting Software Solutions Benefit Singapore Businesses?

Industry-specific accounting software provides features tailored to the unique needs of each sector. Retailers can manage inventory, construction firms can track projects, hospitality companies can automate billing, and manufacturers can control production costs.