Have you ever finalized your fiscal year only to discover discrepancies in your financial statements? These frustrating inconsistencies often stem from overlooked or improperly recorded adjusting entries, which can significantly disrupt your entire accounting process.

In fact, a study focusing on Malaysian companies revealed that inadequate audit quality adversely affects earnings quality, highlighting the critical importance of accurate financial reporting.

In this article, we’ll break down adjusting entries—what they are, why they matter, and how to handle them correctly. Plus, we’ll introduce the best tools to maintain accurate and reliable financial records.

Key Takeaways

|

Table of Content

Content Lists

What are Adjusting Journal Entries?

An adjusting journal entry is a crucial record ensuring accurate financial data.It is recorded before financial statements are issued to reflect necessary adjustments. This process provides a clear and accurate financial overview.

For those in the accounting profession, understanding past adjusting journal entries is vital, as they ensure that each account accurately reflects actual balances. These entries modify account records, aligning revenues and expenses with their corresponding periods, regardless of when cash transactions take place.

To better understand their significance, let’s look at adjusting journal entries examples in real-world scenarios. These include recognizing accrued revenues, allocating deferred expenses, and recording depreciation—all essential processes for maintaining accurate financial records.

By mastering the preparation of adjusting and reversing entries, businesses can generate precise general journal entries, enhancing the accuracy and dependability of financial statements.

Adjusting Journal Entries Function

Adjusting journal entries ensure accurate financial records by recording revenues and expenses in the correct period. They align estimated data with actual figures for transparency. Without them, financial statements may be misleading, impacting decisions and compliance.

Adjusting journal entries bridge recorded transactions and actual business activities. They ensure accurate recognition of expenses and revenues, reflecting true operations. This prevents errors and misstatements, maintaining reliable financial reports.

Mastering adjusting entries improves financial management and ensures compliance. Automation simplifies tracking discrepancies, reducing errors and enhancing efficiency. This helps businesses maintain accurate records for long-term stability.

Why Adjusting Journal Entries is Important?

Adjusting journal entries (AJEs) ensure accurate financial reporting by aligning financial data with actual business activities. They correct discrepancies and uphold accounting principles. AJEs record income and expenses in the proper period, regardless of cash transactions.

Here are a few reasons why AJEs are important:

-

Accurate financial reporting

AJEs ensure accurate financial reporting by aligning revenues and expenses with the correct period. They help financial statements reflect a true picture of a business’s health. This accuracy supports informed decision-making and compliance with accounting standards.

-

Compliance with accounting standards

Most accounting frameworks, such as Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), mandate the use of adjusting journal entries. These adjustments help businesses maintain compliance with financial regulations and ensure that financial statements are prepared according to standardized principles.

-

Accounting automation

Accounting automation simplifies adjusting entries by minimizing errors and ensuring systematic record-keeping. It streamlines reconciliation, saving time while enhancing financial accuracy. This leads to more reliable and efficient financial data management.

-

Optimizing tax reporting

Properly adjusted financial records contribute to accurate tax reporting. Adjusting journal entries help businesses recognize income and expenses in the correct tax period, preventing miscalculations that could lead to overpayment or penalties due to non-compliance with tax regulations.

-

Financial decision-making

Reliable financial records support strategic decision-making by providing accurate profitability insights. They help allocate resources efficiently and plan for growth. Without adjusting entries, financial reports may be misleading.

What is the Purpose of Adjusting Journal Entries?

The purpose of adjusting journal entries is to ensure accurate financial records throughout the accounting cycle. These entries align revenues and expenses with the correct period, even when cash flow timing differs. Adjustments help correct discrepancies in accrued expenses and deferred revenues. This ensures a precise financial overview.

Within the accounting cycle, adjusting entries convert cash-based transactions into an accrual format, ensuring compliance with accounting principles. This process maintains reliable financial statements by tracking revenues and expenses accurately. Without adjustments, financial reports may be misleading, impacting strategic planning and compliance.

Mastering the purpose of adjusting journal entries ensures transparent and accurate accounting records. Proper adjustments enhance financial reporting, support data-driven decisions, and maintain long-term stability. This process helps businesses align transactions with the correct accounting periods.

Key Differences Between Cash Accounting and Accrual Accounting

Choosing between cash and accrual accounting impacts financial reporting, taxes, and business decisions. Each method has unique advantages, depending on business needs. Here are their key differences:

Cash Accounting

- Recognition timing: Transactions are recorded only when cash is received or paid.

- Simplicity: Straightforward and easy to manage, making it ideal for small businesses.

- Financial impact: Can cause income fluctuations based on cash flow rather than actual earnings.

Accrual Accounting

- Recognition timing: Records revenue and expenses when they are earned or incurred, regardless of cash flow.

- Accuracy: Offers a more precise financial picture by including receivables and payables.

- Regulatory compliance: Required for larger companies and publicly traded businesses under GAAP.

Type of Transaction Adjusting Journal Entries

After understanding the definition, function, and purpose of adjusting journal entries, the next step is recognizing the various transaction types. Here are seven key types of accounting journal entries that businesses should be aware of:

-

Equipment

Equipment refers to company-owned assets used in operations, which may be reusable or consumable. Adjustments are made to reflect wear, usage, or loss in value. These entries ensure that asset values remain accurate in financial records.

-

Revenue receivables

Revenue receivables involve sales made on credit, where customers delay payment. Adjusting entries ensure income is recorded in the correct period. This process maintains accurate revenue recognition in financial statements.

-

Accrued expenses (expense debt)

Accrued expenses are costs incurred but not yet paid by the reporting date. These adjustments ensure all expenses are recognized in the appropriate period. Without them, financial statements may understate liabilities.

-

Accrued revenues

Accrued revenues reflect income earned but not yet invoiced or received. Adjusting entries match these earnings to the correct accounting period. This ensures revenue reporting aligns with actual business activities.

-

Deferred revenues (prepaid income)

Deferred revenues refer to payments received before delivering goods or services. Adjustments allocate earned portions over time while deferring unearned amounts. These entries prevent premature revenue recognition.

-

Deferred expenses (expenses paid in advance)

Deferred expenses are costs paid upfront for future benefits, like rent or insurance. Adjusting journal entries distribute these costs across relevant periods. This prevents overstating expenses in one period.

-

Depreciation expenses

Depreciation accounts for asset wear and reduces their book value over time. Adjustments ensure assets are expensed gradually rather than all at once. These entries improve the accuracy of financial reporting.

-

Provisions (loss of accounts receivable)

Provisions account for potential losses from uncollectible receivables. These adjustments reflect realistic asset values, preventing overstated financial positions. This helps businesses anticipate and manage credit risks.

-

Shrinkage and purchase return

Shrinkage represents inventory loss due to damage, theft, or mismanagement. Meanwhile, purchase return transactions record goods sent back to suppliers. Adjusting these journal entries ensures financial statements accurately reflect inventory levels and business costs.

Choosing the right accounting software for adjusting journal entries ensures accuracy and efficiency. With flexible pricing, businesses can access advanced features affordably. Click the banner below to explore available pricing schemes!

Steps to Make Adjusting Journal Entries

Recording and adjusting journal entries is a crucial process in maintaining accurate financial reporting for a business. These entries help correct discrepancies, account for accrued revenues or expenses, and ensure that financial data accurately represents real business activities.

Following a structured approach simplifies the process and guarantees precise financial reporting.

1. Review the trial balance

Before making any adjustments, it is important to review the trial balance to confirm that all financial transactions have been properly recorded in the general ledger. This report serves as a key tool for analyzing and verifying transactions, and using financial management software can help streamline this process.

2. Prepare the adjusting journal entries

The next step involves compiling and recording necessary adjustments for accounts such as income, expenses, and assets. These entries update financial records to reflect actual business activities, ensuring that reports present an accurate financial picture.

3. Update the trial balance and generate financial reports

Once adjustments are recorded, the trial balance is revised to incorporate these changes. This step ensures the accuracy of financial statements such as the income statement, balance sheet, and cash flow statement, providing a clear and reliable financial overview.

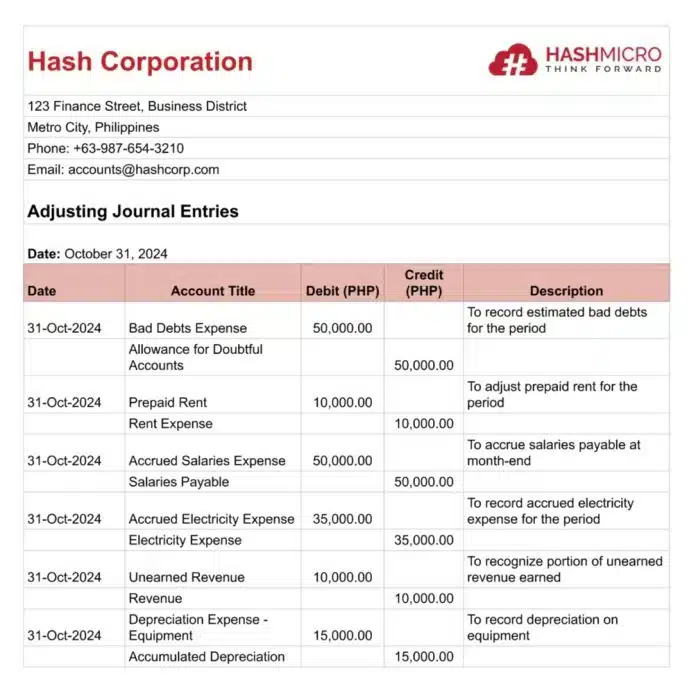

Adjusting Journal Entries Examples

Adjusting journal entries ensure accurate financial records by aligning revenues, expenses, and accounts with the correct period. They help maintain financial transparency and reflect a company’s true financial position. These adjustments follow the matching principle for precise reporting.

To better understand the significance of these adjustments, let’s examine a practical example that demonstrates how adjusting journal entries work and why they are crucial for accurate financial reporting.

Inaccurate financial records can lead to costly errors and misinformed decisions. Try a free demo to see how adjusting journal entries improves accuracy and compliance!

Easily Manage Your Journal Entries with HashMicro’s Accounting Software

HashMicro Accounting Software is the leading solution for businesses in Malaysia looking to optimize their financial management processes. With HashMicro, companies can maintain accurate financial records, reduce manual errors, and achieve better compliance with accounting standards.

For those interested in HashMicro’s accounting software, a free demo is available to explore its advantages. This demo offers a detailed insight into the software’s features and capabilities, demonstrating how it simplifies adjusting entries and enhances overall financial management.

Here are some of the key features provided by HashMicro’s accounting software:

- Hashy AI by HashMicro: streamlines invoice follow-ups, payment tracking, and vendor communication. It predicts payment schedules, sends alerts, and ensures accurate reconciliation. These AI features optimize cash flow and budgeting.

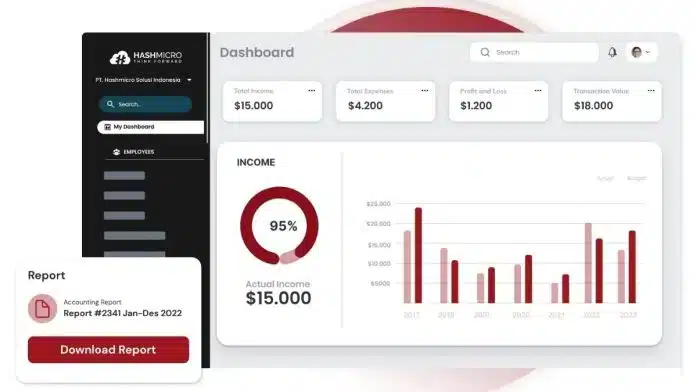

- Financial Dashboard: Gain real-time insights into your company’s financial health by tracking income, expenses, cash flow, and outstanding balances in one centralized platform. This feature helps businesses identify financial trends, monitor performance, and make informed decisions.

- Cash Flow Forecasting: Accurately predict future income and expenses over a specified period, allowing businesses to manage budgets effectively. By analyzing past transactions and financial trends, companies can prepare for potential cash shortages or surpluses.

- Fast Bank Reconciliation: Automatically imports, matches, and categorizes bank transactions, reducing manual data entry and improving accuracy. This feature ensures that financial records align with actual bank statements, preventing errors and discrepancies.

- Accrual & Amortization: Automates the calculation and recording of accruals and amortization, ensuring financial statements reflect true obligations and asset depreciation. This feature helps businesses comply with accounting standards while reducing the risk of misstatements.

- Peppol e-Invoicing: Enables seamless invoice transactions through Malaysia’s Peppol e-Invoicing network, ensuring standardized and secure exchanges. This feature helps businesses improve invoicing efficiency, reduce processing time, and enhance compliance with local regulations.

- Analytical Reporting: Generates financial reports like income statements and balance sheets instantly, aiding better decision-making. Real-time insights help businesses assess performance and plan effectively.

HashMicro offers seamless integration with multiple modules and third-party systems, ensuring flexibility for business needs. With customizable options, it provides a tailored accounting solution, making it ideal for businesses seeking adaptability.

Conclusion

Adjusting journal entries play a crucial role in ensuring accurate financial records for your business. This process involves modifying account balances at the end of the accounting cycle to maintain precision in financial reporting.

The main objective of these entries is to recognize income and expenses that were not initially recorded during the reporting period. Proper adjustments are essential, as errors in financial data can lead to significant discrepancies in future accounting periods.

Utilizing reliable accounting software in Malaysia can streamline financial record management. With advanced features, a user-friendly interface, and automated error detection, HashMicro’s Accounting Software helps businesses improve financial accuracy and prevent fraud.

Effective financial management starts with the right tools—discover the best accounting software in Malaysia or request a free demo today!

Questions About Adjusting Journal Entries

-

What are the main rules for adjusting entries?

Adjusting entries must follow the matching principle, ensuring revenues and expenses are recorded in the period they occur. They should be based on accurate accrual accounting, properly documented, and reviewed for compliance with accounting standards like GAAP or IFRS.

-

How do you correct journal entries?

To correct journal entries, follow these steps:1. Identify the Error – Review financial records and the trial balance to locate incorrect entries.2. Determine the Correction Method – Choose one of the following:

– Reversing Entry: If the error is discovered before financial statements are finalized, create a reversing entry to negate the incorrect transaction.

– Adjusting Entry: If the incorrect amount was recorded, adjust the affected accounts with an additional journal entry.

– Correcting Entry: If the mistake involves the wrong accounts, make a new journal entry to transfer the amount to the correct accounts.

3. Record the Correction – Ensure the correcting entry includes proper debits and credits to maintain accuracy.

4. Review and Verify – Check financial statements after adjustments to confirm correctness and compliance with accounting principles. -

How to make adjusting journal entry?

– Review the trial balance to identify unrecorded revenues or expenses.

– Determine necessary adjustments based on accrual accounting principles.

– Record the adjusting entries in the general journal, ensuring correct debit and credit accounts.

– Post to the ledger and update financial statements for accuracy.

{kind=link}