Running a business often feels like juggling way too many things at once, doesn’t it? From tracking cash flow to managing bookkeeping and keeping inventory in check, things can get overwhelming fast, especially without the right systems in place.

That’s why having a reliable accounting system is so important. It keeps your records accurate and helps prevent costly mistakes, while giving you clear insights into your business’s performance and growth.

If you’re not yet familiar with the basics of bookkeeping, don’t worry! This article breaks it down for you. Then, we’ll introduce a smart tool that not only records transactions accurately, but does a whole lot more to support your business. Are you curious already? Keep reading to find out!

Key Takeaways

|

Table of Content

Content Lists

What is Bookkeeping?

Bookkeeping refers to the consistent recording of a company’s financial activities. Accurate bookkeeping helps businesses monitor their financial records and supports informed decisions related to operations, investments, and funding.

They are responsible for maintaining a company’s financial data. Without them, businesses would struggle to understand their financial standing and track internal transactions.

Typical bookkeeping duties include:

- Issuing invoices for sales

- Logging and organizing incoming payments

- Reviewing and processing supplier invoices

- Making payments to vendors

- Managing payroll

- Compiling financial statements

Today, traditional bookkeeping methods have been mostly replaced by digital tools and software, which help streamline tasks and improve accuracy. To understand the full role of bookkeeping, it’s worth exploring how it fits into broader financial practices.

Types of Bookkeeping

Bookkeepers typically use one of two main methods to record transactions: single-entry or double-entry bookkeeping.

- Single-entry bookkeeping records each transaction only once, usually in a single line. It’s commonly used for basic tasks like tracking cash flow, taxable income, and deductible expenses.

- Double-entry bookkeeping, on the other hand, records each transaction twice—once as a debit and once as a credit. This method follows the accrual accounting system and helps manage a company’s assets, liabilities, equity, income, and expenses more accurately.

While single-entry is simpler and easier to manage, double-entry provides a more complete picture of a company’s finances and helps reduce accounting errors.

What Does a Bookkeeper Do?

A bookkeeper is a financial specialist responsible for recording a business’s daily transactions, such as sales, purchases, payroll, accounts receivable, and accounts payable. They help track the flow of money in and out of the business by keeping detailed and organized financial records.

Unlike accountants, bookkeepers usually don’t hold formal accounting certifications. Their main role is to enter and manage transaction data within an accounting system.

The exact duties of a bookkeeper can vary depending on the company’s size and needs. Bookkeepers may work for large corporations, small businesses, or independently as freelancers. Some of their key responsibilities include:

- Recording transactions using accounting software, spreadsheets, or databases

- Managing financial documents like bank statements, cash flow records, and profit-and-loss reports

- Creating invoices and handling incoming payments

- Tracking account debits and credits

- Reconciling bank and financial statements

- Compiling balance sheets and income statements

- Checking financial reports for accuracy

- Overseeing payroll processes

- Preparing and submitting tax returns on behalf of the business

Why is Bookkeeping Important?

Accurate bookkeeping gives businesses a dependable way to evaluate their performance. It also provides essential data for making strategic decisions and tracking progress toward income and revenue goals.

In short, maintaining organized financial records becomes vital once a business starts operating, even if it requires additional time and investment.

Because hiring a full-time accountant can be costly, many small businesses choose to employ a bookkeeper or outsource the work to a professional service. It’s also common for new business owners to underestimate the importance of tracking every financial transaction, which can lead to issues later on.

Many modern SMEs in Malaysia now rely on financial management software to maintain accurate records, monitor expenses, and generate real-time reports.

Activities in Bookkeeping

To maintain accurate and organized financial records, bookkeepers carry out a variety of important activities. These tasks go beyond simply recording transactions, as they aim to organize financial data.

Below are some of the key responsibilities typically handled by bookkeepers.

- Financial Reports: Bookkeepers create essential reports such as the balance sheet, income statement, and cash flow statement to give a clear picture of the business’s financial health.

- Invoices and Payments: They handle billing by creating and sending invoices to customers, tracking incoming payments, and following up to ensure they’re received on time. They also review supplier invoices for accuracy and make sure payments are made promptly.

- Payroll and Taxes: Bookkeepers calculate employee wages, including deductions for taxes, leave, and retirement contributions. They also prepare and file tax documents such as payroll tax and sales tax returns.

In addition, bookkeepers may support tasks like budgeting, financial forecasting, and compiling annual financial summaries.

Accrual vs Cash-Basis Bookkeeping

There are two commonly used accounting methods for managing small business bookkeeping effectively: the cash basis and the accrual basis.

The key difference between them lies in the timing of when sales and expenses are recorded in the accounting records.

1. Cash Basis of Accounting

This method records income only when cash is received and expenses only when they are paid. It focuses purely on cash flow, making it straightforward and easier for smaller operations to manage.

- No tracking of prepaid or outstanding items like accrued income or unpaid expenses

- Shows lower income on financial statements since it only includes completed transactions

- Provides a short-term view of financial health

- Better reflects liquidity, you know exactly how much cash is available

- Taxes are paid only on money that has actually been received

- Best suited for small businesses and sole proprietors with no inventory

- Very easy to use, as it focuses only on cash in and out

- Accrual Basis of Accounting

In contrast, the accrual method records revenues and expenses when they are earned or incurred, regardless of when the cash is actually received or paid.

- Includes prepaid expenses, outstanding bills, and unearned revenue

- Shows higher income on financial reports as it accounts for all earned revenue

- Provides a long-term, realistic view of business performance

- May show profitability even when cash is low, as it doesn’t track cash movement directly

- Taxes must be paid even on income that hasn’t been collected yet

- Required for businesses with revenues over $5 million annually

- More complex to manage, as it involves additional tracking and adjustments

Proper bookkeeping supports effective cash flow management, which helps businesses avoid shortages and plan for growth more confidently.

Bookkeeping vs. Accounting: What’s the Difference?

Understanding the difference between bookkeeping and accounting is essential for any business owner. While the two are closely related, they serve different purposes and require different skill sets.

So, what are the differences? Here are several key differences:

- Role in Financial Management: Bookkeeping acts as the foundation for accounting. Once financial transactions are recorded through bookkeeping, accounting begins by analyzing that data.

- Nature of Work: Bookkeeping is more clerical, often automated by systems and tools. Accounting is more analytical and decision-focused.

- Determining Financial Health: Bookkeeping alone can’t give you a full picture of a business’s financial position. Accounting helps assess financial performance through reports and statements.

- Financial Statements: While bookkeeping does not include the preparation of financial statements, accounting relies heavily on them, like profit and loss reports, balance sheets, and cash flow statements, to evaluate business health.

- Methods and Tools: Bookkeepers use tools such as journals, ledgers, and trial balances. In contrast, accountants work with comprehensive statements and reports like income statements, balance sheets, and cash flow statements.

- Decision-Making Support: Bookkeeping doesn’t directly support business decision-making. Accounting, however, plays a crucial role in helping stakeholders make informed decisions based on financial insights.

- Approaches and Specializations: Bookkeeping uses single-entry or double-entry systems. Accounting includes specializations such as financial accounting, cost accounting, and management accounting, depending on business needs.

Implementation of Bookkeeping

In Malaysia, many businesses have adopted bookkeeping or cost accounting practices as part of their daily operations. However, it’s important to remember that each business has its own unique accounting cycle.

So, how do different industries apply these accounting methods? Let’s take a closer look at some examples:

1. Service Companies

Service-based businesses typically have simpler operations, as they focus on delivering services rather than physical goods. Their process usually involves preparing the service and receiving payment from clients.

Because of this, their financial reports mainly highlight the cost of services rendered to customers.

2. Manufacturing Companies

Manufacturing businesses handle the production of goods, starting from raw materials and ending with finished products ready for sale. As a result, cost accounting in this sector primarily revolves around calculating the selling price of products.

It also provides detailed insights into the production cost of each unit stored in the warehouse.

3. Trading Companies

Trading companies buy and sell goods without producing them. They act as distributors, either directly or through intermediaries. For these businesses, the accounting process includes tracking goods entering and exiting inventory.

They must also manage accounts related to cost of goods sold (COGS), stock levels, discounts, markdowns, and other retail-specific factors.

In fast-moving sectors like fashion, accurate bookkeeping is especially important. Every purchase and sale transaction must be properly recorded to maintain financial clarity and avoid discrepancies.

You can also review standard bookkeeping practices to see how they’re applied across different industries.

How to Set Up Bookkeeping for Business

To properly implement the bookkeeping process in your business, you’ll need to go through the following steps:

1. Open a Business Bank Account

Start by opening a dedicated checking account for your business. This helps you manage your company’s finances in an organized manner.

2. Separate Business and Personal Finances

Keep your business expenses completely separate from your personal ones. Mixing the two can create confusion and make tax filing much more stressful later on.

3. Choose a Bookkeeping Method

Select between the single-entry and double-entry bookkeeping systems.

- If you’re just starting out, the single-entry system may be more suitable since it records each transaction once, either as income or expense, while tracking assets and liabilities separately.

- For more comprehensive financial tracking, the double-entry system is preferred. It records every transaction in at least two accounts (one debit and one credit) offering a more accurate and balanced view of your business finances.

4. Select an Accounting Method

Decide whether to use the cash basis or accrual basis of accounting.

- Many small businesses begin with the cash basis because it’s simple and doesn’t require tracking accounts receivable or payable.

- However, the accrual basis is widely used because it gives a more accurate picture of business performance by recording revenues and expenses when they are earned or incurred, not when cash changes hands.

5. Use the Right Tools to Categorize Transactions

Utilize proper tools to categorize all transactions into relevant groups such as assets, liabilities, income, expenses, and equity. You can use cloud-based software, or rely on spreadsheets and Excel templates, whichever works best for your business size and needs.

6. Categorize Transactions Consistently

Make it a habit to record and categorize transactions regularly. Accurate records support better financial decisions and make it easier to identify valid tax deductions during filing.

7. Store Financial Documents Digitally

Use digital tools to store important financial documents, like receipts, invoices, and records—so you won’t be scrambling to gather everything at tax time. This also helps with long-term organization and compliance.

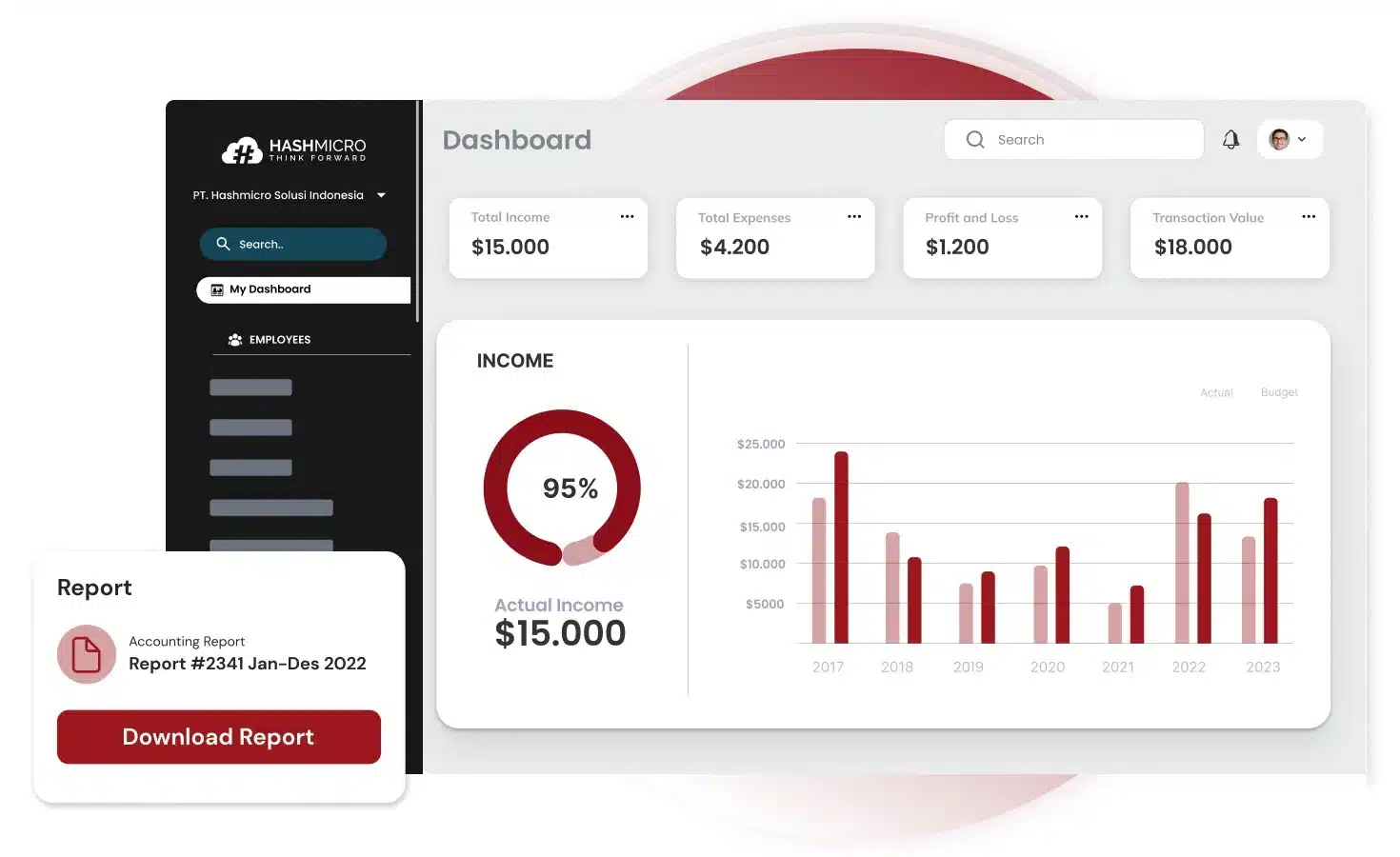

Simplify Your Bookkeeping with HashMicro’s Smart Accounting Software

Managing business finances shouldn’t be a headache, especially when you’ve got other things to focus on. With HashMicro’s integrated accounting software, any companies and organizations can their entire financial workflow from one central system.

Whether you’re handling day-to-day operations or preparing for audit season, here’s how HashMicro helps you stay ahead:

- LHDN-Compliant Reporting: Generate accurate, real-time financial reports that simplify tax submissions and help you stay aligned with Malaysia’s regulatory requirements.

- Full-Suite Billing & Invoicing Tools: From quotations to debit notes and billing, handle everything in one system; no more jumping between spreadsheets or apps.

- Multi-currency Transactions: Doing business across borders? Our system makes it easy to record and convert multiple currencies with automatic exchange rate updates.

- Live Cash Flow Monitoring: Stay on top of your business’s financial health with direct and indirect cash flow reports. Track inflows and outflows without manual work.

- Flexible Budget Management: Easily assign, monitor, and control budgets across teams, branches, or projects, ensuring accountability at every level.

On top of that, HashMicro’s accounting software connects seamlessly with modules like sales, inventory, procurement, and HR, so all your financial data lives in one ecosystem. Faster decisions, fewer errors, and way less admin stress.

Conclusion

Bookkeeping is the process of recording and organizing financial transactions to keep your business financially healthy. It helps business owners track income, manage expenses, and make informed financial decisions every step of the way.

If you’re tired of spreadsheets and manual work, HashMicro’s accounting system can simplify everything for you. From invoicing to reports, you get full control of your business finances in just a few clicks.

Stay compliant, save time, and get real-time insights. HashMicro helps your business grow smarter, not harder. Start your free demo today and see how easy bookkeeping can actually be!

FAQ on Bookkeeping

-

What qualifications are needed to become a bookkeeper in Malaysia?

In Malaysia, many entry-level bookkeeping jobs only require an SPM certificate. But if you want to stand out, it’s a good idea to take additional courses like the AAT Foundation Certificate in Bookkeeping or the Sijil Kemahiran Malaysia (SKM) Level 3 in Accounting. Some employers also prefer candidates with a diploma in accounting or those affiliated with local professional bodies such as MACBA.

-

What are some common bookkeeping mistakes Malaysian businesses make?

A lot of local businesses—especially small ones—fall into the trap of treating bookkeeping as an afterthought. Common mistakes include not reconciling bank statements regularly, mixing personal and business expenses, misclassifying transactions, and missing deadlines for SST filings or LHDN requirements. These issues can lead to audit headaches or even tax penalties.

-

How often should I update my business records?

If you’re running a business in Malaysia, it’s best to update your financial records at least once a month. This keeps your cash flow clear, makes tax season less stressful, and helps you make better decisions throughout the year. For businesses with higher transaction volumes, weekly or even daily updates are ideal.