The general ledger serves as the backbone of financial accounting; however, many businesses fail to recognize the complexities involved in its proper management. From tracking assets to managing liabilities, a comprehensive ledger is vital to ensure accurate financial records.

However, one of the biggest concerns for managers is the potential for errors and inconsistencies within the general ledger. These discrepancies can lead to faulty financial statements, audits, and missed opportunities for optimization and growth.

According to a report by PwC Malaysia, many companies continue to rely on outdated manual methods to manage their general ledgers, which makes them more prone to errors and delays in financial reporting. This reliance on traditional systems hampers efficiency and increases the risk of non-compliance with financial regulations.

Continue reading to discover how the right strategies and accounting software can help you optimize your general ledger management. By leveraging modern tools, businesses can ensure accuracy, streamline processes, and remain compliant with industry standards.

Table of Content

Content Lists

Key Takeaways

|

What is a General Ledger?

A general ledger (GL) is the central record-keeping system for a company’s financial transactions, where all debit and credit entries are tracked and organized. It is the foundation of accounting, serving as the primary source for preparing trial balances and financial statements, ensuring accuracy in financial reporting.

Each general ledger account summarizes a specific type of transaction, such as assets, liabilities, equity, revenues, or expenses. Maintaining detailed records like transaction dates, descriptions, and amounts provides a clear and organized view of a company’s financial health over time.

The general ledger is essential for monitoring finances, tracking cash flow, and ensuring tax compliance. It also helps prevent errors and fraud, making it a vital tool for businesses to compile accurate and reliable financial data for reporting and informed decision-making.

The Importance of General Ledger Accounts?

Businesses use general ledger accounts to monitor their financial performance and ensure overall financial health. By categorizing transactions into specific accounts such as assets, liabilities, revenues, and expenses, companies can gain a clearer view of their financial standing and identify areas of improvement.

A well-maintained general ledger provides a comprehensive record of all financial activities, enabling businesses to track cash flow, manage budgets effectively, and generate accurate financial reports. These insights help managers make informed decisions and ensure compliance with tax regulations and accounting standards.

In addition, the general ledger serves as a vital tool for preventing errors and fraud. By organizing and verifying transactions, businesses can quickly detect discrepancies, ensuring the integrity of their financial data and maintaining transparency across the organization.

Functionality of a General Ledger

The general ledger (GL) plays a key role in tracking and organizing all of a company’s financial transactions. Here’s how it works in a typical accounting cycle:

1. Transaction recording in journals

All financial transactions begin by being recorded in the journal. Each journal entry includes a date, description, and the amount involved in the transaction, with the corresponding debits and credits.

These transactions are typically categorized under various accounts, such as sales, expenses, or cash. Once recorded, these journal entries are then posted to the general ledger for further processing.

2. Posting to the general ledger

After transactions are recorded in the journal, they are transferred to the general ledger accounts. Each account in the general ledger represents a specific category, such as assets, liabilities, or equity.

The amounts are posted to the corresponding accounts, maintaining the principle of double-entry accounting, where each debit has an equal and opposite credit. This ensures that the accounting equation (Assets = Liabilities + Equity) is balanced.

3. Trial balance preparation

Once all transactions are posted to the general ledger, a trial balance is created to verify the accuracy of the ledger. This step ensures that the total of all debits equals the total of all credits. Any discrepancies between debits and credits indicate errors that need to be resolved before proceeding with financial statement preparation.

4. Generating financial statements

The final step in the general ledger process is using the general ledger data to prepare financial statements. Information from the general ledger (GL) accounts, such as revenue, expenses, and assets, is used to compile the balance sheet, income statement, and cash flow statement.

These reports offer businesses a clear overview of their financial performance, providing essential information for informed decision-making and regulatory compliance.

Categories of General Ledger Accounts

The general ledger organizes financial transactions into several key categories, each providing vital insights into a company’s financial health. These categories include assets, liabilities, equity, revenues, and expenses, and each plays a distinct role in the accounting process.

- Assets: Assets represent what a company owns or controls that has monetary value. They are classified into current assets (such as cash and accounts receivable) and non-current assets (like property and equipment), which help businesses evaluate their ability to generate income.

- Liabilities: Liabilities are obligations that a company owes to external parties, such as loans, accounts payable, and accrued expenses. Managing liabilities is essential for businesses to ensure they can meet financial obligations and avoid liquidity issues.

- Equity: Equity reflects the ownership interest in a company, representing the difference between assets and liabilities. It includes invested capital, retained earnings, and shareholder equity, which are crucial for understanding a company’s net worth and financial stability.

- Revenues: Revenues represent the income generated from the sale of goods or services. Tracking revenues is crucial for measuring business performance, assessing profitability, and pinpointing areas for growth and expansion.

- Expenses: Expenses are the costs incurred in the process of generating revenue, such as rent, salaries, and materials. Monitoring expenses allows businesses to manage costs efficiently, improve profitability, and maintain a healthy bottom line.

Each category in the general ledger offers unique insights into a company’s financial performance, helping businesses make informed decisions and maintain financial health. Understanding these categories is fundamental to effective financial management and reporting.

Additional Types of General Ledger Accounts

In addition to the primary general ledger accounts, other specialized accounts serve distinct purposes, such as contra accounts and temporary accounts. These accounts play key roles in providing a more detailed and accurate financial picture, ensuring transparency and proper financial reporting.

-

Contra accounts

Contra accounts are used to offset the balances of related accounts in the general ledger. For example, the accumulated depreciation account is a contra asset account that reduces the value of a fixed asset, such as equipment or property.

By maintaining contra accounts, businesses can track reductions in asset values and more accurately represent the current worth of their assets.

-

Temporary accounts

Temporary accounts are used to track financial transactions over a specific period, typically within a fiscal year. These accounts include revenues, expenses, gains, and losses, and are reset at the end of each accounting period.

The balances in these accounts are transferred to the retained earnings account in the equity section of the general ledger, ensuring that financial statements reflect the current financial performance of the business.

-

Income statement accounts

Some general ledger accounts are directly linked to the income statement, summarizing revenues and expenses. For instance, accounts receivable track money owed to the business, while accounts payable track money the company owes.

These accounts, often broken down by departments or business units, provide detailed insight into income and expenses, helping businesses monitor profitability and financial health.

-

Balance sheet accounts

Other general ledger accounts correspond to the balance sheet, summarizing assets, liabilities, and equity. These accounts include cash, inventory, and long-term liabilities, and help businesses assess their financial position at any given time.

These accounts are critical for understanding the company’s ability to meet financial obligations and manage resources effectively.

By incorporating contra accounts and temporary accounts into the general ledger, businesses ensure their financial records are comprehensive, accurate, and ready for financial reporting. These additional accounts provide more transparency, helping businesses better track the value of assets, manage income and expenses, and maintain overall financial control.

Connection to Double-Entry Bookkeeping

The general ledger plays a crucial role in double-entry bookkeeping, which ensures that every financial transaction is accurately recorded. In this system, each transaction is entered twice—once as a debit and once as a corresponding credit—to maintain the accounting equation’s balance (Assets = Liabilities + Equity).

Each debit and credit in the general ledger must offset one another, ensuring that the sum of all debits equals the sum of all credits. For instance, when recording a sale, the cash account is debited, and the revenue account is credited, ensuring that the financial records remain balanced and accurate.

The double-entry system, backed by the general ledger, provides a built-in check against errors, as any imbalance between debits and credits will indicate an issue. By following this method, businesses can maintain reliable financial records and produce accurate financial statements, fostering transparency and financial integrity.

Reconciling the General Ledger

General ledger reconciliation is a critical process for ensuring the accuracy and integrity of financial data. At the end of each fiscal period, accountants calculate a trial balance by listing all debit and credit accounts, comparing their totals to verify that the two are equal.

While a balanced trial does not guarantee error-free records, the reconciliation process helps identify discrepancies, such as missing journal entries or unrecorded debits and credits. By carefully reviewing and comparing the accounts, businesses can correct errors and ensure financial data is accurate and reliable for reporting.

Reconciliation of the general ledger is essential for maintaining confidence in financial statements and ensuring that all transactions are properly accounted for. It also plays a key role in preventing fraud and improving the efficiency of financial operations, ultimately contributing to better decision-making and compliance.

Accounting Software for General Ledgers

The advent of accounting software has revolutionised the management of general ledgers, transitioning from manual paper records to automated systems. These software solutions integrate various business processes with accounting functions, ensuring that general ledger accounting is efficient and accurate.

One of the major benefits of using accounting software for managing the general ledger is its ability to streamline and automate essential accounting tasks. This reduces the risk of errors, improves data accuracy, and saves significant time compared to manual processes.

Key features of accounting software include:

Bank reconciliation: Automatically match bank transactions with recorded entries in the GL for quick reconciliation.

- Financial reporting: Generate accurate, real-time financial reports such as balance sheets, income statements, and cash flow statements.

- Accounts receivable and payable: Manage outstanding debts and liabilities efficiently, improving cash flow management.

- Tax preparation: Simplify tax filing with automated calculations based on your accounting records.

- Workflow automation: Automate routine accounting tasks to increase efficiency and reduce manual intervention.

Additionally, accounting software ensures seamless integration with other business systems, such as customer relationship management (CRM), payroll, and e-commerce platforms. This connectivity enables businesses to manage financial data alongside other operational areas, ensuring smoother workflow and better decision-making across departments.

Furthermore, modern accounting software often comes with mobile applications, allowing users to access financial data on the go. With real-time access to reporting, analytics, and compliance features, businesses can ensure greater transparency, improve audit capabilities, and stay aligned with regulatory requirements.

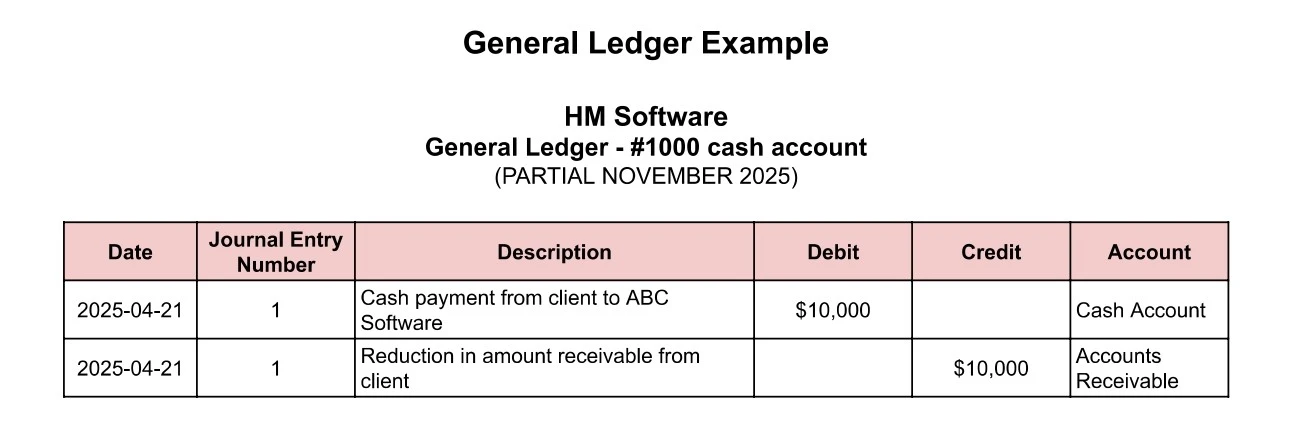

Example of a GL Transaction

The general ledger is the central record of a company’s financial transactions, summarizing all business activities, including debits and credits across various accounts. Using general ledger templates helps ensure accurate transaction recording and provides a clear financial overview for reporting and analysis.

Below is an example using the cash account of HM Software to illustrate how a general ledger works:

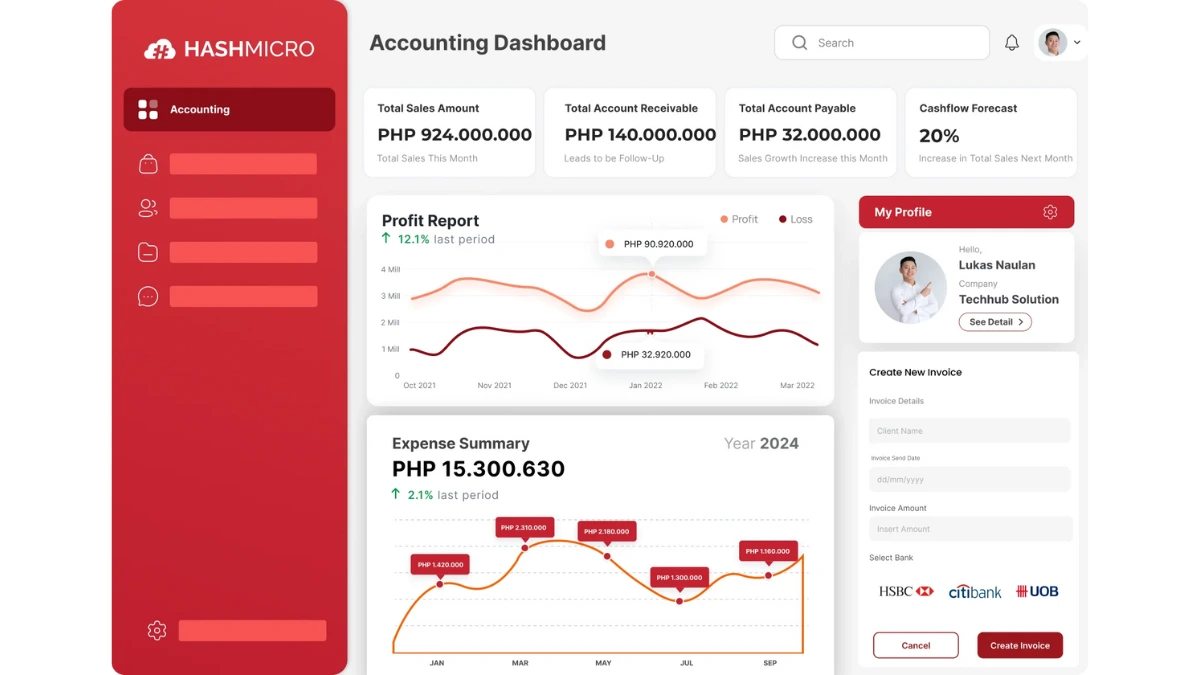

Streamline Your General Ledger Management with HashMicro Accounting Software

HashMicro is a leading accounting software solution known for its efficient management of general ledgers. Established in Singapore, HashMicro has expanded its reach to serve businesses worldwide, including those in Malaysia.

Why we choose HashMicro: We choose HashMicro for its flexibility and integration capabilities, which ensure that businesses can manage their general ledger seamlessly while maintaining compliance with industry regulations.

Ready to streamline your accounting processes? Reach out to HashMicro’s expert team or request a free demo to experience how this solution can help your company stay compliant and improve financial operations.

HashMicro’s accounting software is renowned for its comprehensive suite of features, tailored to meet the diverse needs of businesses. Below are some of the key features of the HashMicro Accounting solution:

- Bank Integrations – Auto Reconciliation: By automatically reconciling bank transactions with general ledger accounts, discrepancies are quickly identified and corrected. This leads to more accurate financial data and saves time spent on manual reconciliation.

- Multi-Level Analytical Reports: By comparing financial statements across different projects or branches, businesses gain deeper insights into their performance. This enables more informed decision-making and highlights areas for improvement.

- Profit & Loss vs Budget & Forecast: Tracking and comparing actual performance against budget and forecasted figures ensures financial control. This helps businesses identify variances early and take corrective actions to stay on target with financial goals.

- Cash Flow Reports: Detailed cash flow reports provide a clear view of liquidity, allowing businesses to understand where funds are being allocated. This leads to improved cash flow management and ensures that the business has sufficient resources for its operations.

- Financial Statement with Budget Comparison: Generating comprehensive financial statements that include budget comparisons ensures actual figures align with expected goals. This promotes accountability and helps businesses stay aligned with their financial objectives.

- Multi-Company with Intercompany Transactions and Consolidation: Managing financial data across multiple companies with intercompany transactions and automatic consolidation simplifies reporting and coordination. This ensures the provision of accurate and timely financial information for informed decision-making at a consolidated level.

- Custom Printout for Invoices: Customizing invoice printouts allows businesses to adapt their invoicing to different customer needs and formats. This flexibility enhances professionalism and improves customer satisfaction through tailored communication.

- Chart of Accounts Hierarchy: Organizing the chart of accounts in a structured hierarchy provides clear categorization of financial data. This results in better financial oversight, making it easier to analyze and report on various business activities.

HashMicro stands out as the perfect solution for businesses in Malaysia looking to optimize the accuracy and efficiency of their general ledger management. With customizable features, powerful automation tools, and seamless integrations, HashMicro helps businesses stay organized and compliant with financial regulations.

Conclusion

The general ledger is essential for gaining a clear overview of a company’s financial position by categorizing assets, liabilities, equity, revenues, and expenses. This level of organization enables businesses to track performance, make strategic decisions, and ensure compliance with industry standards.

By leveraging HashMicro’s accounting software, businesses can streamline their general ledger management with automated processes, reducing manual errors and saving valuable time. With features like real-time financial reporting and seamless integration across departments, HashMicro empowers businesses to maintain accurate financial records and optimize their operations.

HashMicro offers the ideal solution for businesses seeking to streamline their general ledger management. Request a free demo today and see firsthand how HashMicro’s software can streamline your accounting processes, improve accuracy, and drive financial efficiency.