Ever feel like you’re drowning in receipts, unsure if every peso is tracked? It’s stressful, right? That’s where a ledger account comes in, it’s like a reliable friend that quietly records the money you make or spend, so you always know where your money goes.

But why stop at just a simple ledger when you can have so much more? You can try HashMicro’s Accounting Software to take things to the next level. It doesn’t just track your transactions; it also automates, organizes your records, and keeps everything accurate and BIR-compliant. Download a free ledger account template now.

Imagine having all your transactions in one simple place without the stress. With a good ledger, even a pile of records can be easy to handle. Want to see how it works and how it can make business simpler? Let’s dive in and get your finances organized!

Key Takeaways

|

Table of Contents

What is Ledger in Accounting?

In accounting, a ledger is a comprehensive record that summarizes all financial transactions within a business. It consolidates data from different accounts, including assets, liabilities, revenues, and expenses, to present an organized financial snapshot.

The ledger acts as the backbone of the accounting system, supporting accurate financial reporting. Categorizing and recording every transaction, including those in the special journal, helps businesses track their financial status and prepare crucial financial statements, like balance sheets and income statements.

Using comprehensive Accounting platforms used locally can make ledger management even more efficient and error-free. With automation, businesses can record transactions more easily and generate real-time financial reports more easily.

Functions of a Ledger

Ledgers play a crucial role in the accounting process by providing a structured way to manage financial data. They serve as the foundation for organizing and tracking financial transactions, ensuring accurate and timely record-keeping.

Some of the commonly known functions of a ledger are:

- Summarizing Financial Data: Ledgers consolidate transaction data from general journals, creating a single reference point for all transactions within a specific period.

- Classifying Transactions: By categorizing transactions, ledgers display the current state of each account, helping businesses understand the status of assets, liabilities, and equity.

- Providing a Basis for Financial Statements: Ledgers organize financial data, making it easier to compile reports such as balance sheets and income statements.

- Supporting Financial Management Systems: Automated systems utilize ledgers to efficiently track transactions, allowing for real-time financial management, particularly for businesses with high transaction volumes.

In sum, ledgers are indispensable in the accounting process, as they organize and categorize data for easy access and reporting. Whether through manual or automated systems, they ensure businesses have an accurate financial picture at any time.

Types of Ledgers

Effectively managing financial records starts with understanding the different types of ledgers. Each type serves a unique purpose, offering insights into various financial aspects of a business. Here are the main types of general ledger:

| Types | Definition |

| General Ledger | Records all financial transactions over a set period. It includes accounts like cash, receivables, and expenses for a broad financial view. |

| Subsidiary Ledger | Provides detailed records for specific transactions, such as receivables or payables. It extends the general ledger for closer transaction tracking. |

| Debtors Ledger | Tracks debts owed by customers to the business. It shows customer balances to monitor credit sales. |

| Creditors Ledger | Monitors amounts owed to suppliers. It lists suppliers offering credit, aiding in managing obligations effectively. |

Incorporating these ledgers into your accounting system enhances accuracy and organization, enabling clear financial insights. Each type plays a role in ensuring a well-rounded, detailed view of your business’s financial health.

Example of Ledger

Creating a ledger requires familiarity with the Chart of Accounts (CoA). Each account in the general ledger is assigned a unique identifier, making it easier to track and update.

Example of a Chart of Accounts (CoA)

Using T-Accounts in Ledger Accounting

A T-account format helps visualize the balance and activity within each account. For instance, a cash account under a T-account setup displays increases and decreases, helping businesses easily track cash flow.

Sample General Ledger Entry

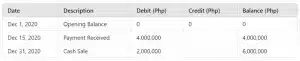

Consider the following transactions for Aksara Gemilang, Inc.:

- Sales on Credit: On December 1, 2020, Aksara Gemilang, Inc. sold goods on credit worth Php 4,000,000 and Php 3,500,000 to two different customers.

- Purchase on Credit: On December 5, 2020, Aksara Gemilang, Inc. purchased office supplies on credit for Php 1,500,000.

- Payment Received: By December 15, Aksara Gemilang, Inc. received a repayment of Php 4,000,000 from the first customer.

- Cash Sale: On December 31, 2020, Aksara Gemilang, Inc. made a cash sale worth Php 2,000,000.

The example would be:

By recording these transactions in the ledger, Aksara Gemilang, Inc. can track and summarize all activity by account. This data will later contribute to generating financial statements.

Free Accounting Ledger Template

An accounting ledger template is a structured tool that records all financial transactions, including income, expenses, and account balances. It ensures your books are accurate, compliant, and ready for financial reporting.

This template is ideal for managing everyday accounting tasks, such as tracking expenses and preparing financial statements. Whether you’re a small business owner or part of a larger organization, this tool simplifies your bookkeeping process.

Conclusion on Example of Ledger

A well-maintained ledger is essential for managing finances accurately and avoiding costly errors in reporting. By categorizing and summarizing transactions, ledgers help businesses gain a clear financial overview at any time. For companies handling large transaction volumes, automated systems make ledger management faster.

With HashMicro’s Accounting Software, you can streamline your ledger processes and get real-time insights into your financial health. This software simplifies complex financial tracking, letting you focus on growing your business confidently. Try the free demo and experience smarter financial management today!

FAQ Around Example of Ledger

-

What is a ledger and examples?

A ledger is a financial record that tracks all transactions within accounts like assets, liabilities, and revenue. Examples include a general ledger for all transactions and a subsidiary ledger for specific accounts.

-

How to write ledger account?

To write a ledger account, record each transaction’s details, including date, account name, debit, and credit amounts. Use T-accounts to organize entries, showing balances on each side.

-

How to solve ledger account?

To solve a ledger account, total both debit and credit sides to find the account balance. Adjust any discrepancies to ensure accuracy in financial statements.