International Financial Reporting Standards (IFRS) are a set of global accounting guidelines designed to make financial statements clear, consistent, and comparable across borders. For businesses in the Philippines, these standards help align reporting practices with what international partners and investors expect.

Using IFRS can strengthen credibility, improve transparency, and make financial information easier for global stakeholders to understand. It supports better decision-making internally while also building trust externally.

Still, adapting reports, processes, and internal understanding to meet international frameworks can feel complex at first. How does IFRS work in practice, and what should businesses prepare before adopting it? Let’s explore the fundamentals, the advantages, and the key considerations to keep in mind.

Key Takeaways

|

Table of Contents

What are International Financial Reporting Standards?

IFRS (International Financial Reporting Standards) are global accounting standards set by the IASB to ensure consistency and transparency in financial reporting. They are used by publicly accountable entities (e.g., listed companies, banks, and insurers) to ensure the credibility of financial statements.

For Filipino businesses, especially those involved in cross-border transactions or seeking foreign investment, following PFRS is crucial. Since PFRS is based on IFRS, businesses can produce reports that meet global standards, making it easier to build trust.

This alignment helps businesses integrate seamlessly into the global market by offering consistent financial information that meets international expectations. Proper adherence to these standards not only improves credibility but also increases access to international growth opportunities.

History of IFRS

The International Financial Reporting Standards have undergone significant evolution over the decades, shaping the global landscape of financial reporting. Understanding its historical journey and how it was adopted in the Philippines through the Philippine Financial Reporting Standards highlights the importance of standardized accounting practices.

Key Milestones:

- 1973: The International Accounting Standards Committee (IASC) was formed to establish global accounting principles.

- 2000: IOSCO endorsed IFRS for cross-border securities offerings, boosting global acceptance.

- 2001: The International Accounting Standards Board (IASB) replaced the IASC, taking over the development and refinement of IFRS.

- 2002: The European Union mandated IFRS for all publicly listed companies by 2005, solidifying IFRS as the global standard.

- 2005: The Philippines adopted IFRS under PFRS, aligning closely with global practices while ensuring local relevance.

- Present: PFRS, governed by the Philippine SEC, remains the mandatory framework for publicly accountable entities, promoting transparency and global alignment.

The historical development of IFRS and its adoption through PFRS in the Philippines demonstrate a commitment to global financial integrity. For Filipino businesses, complying with PFRS ensures credibility and competitiveness in both local and international markets.

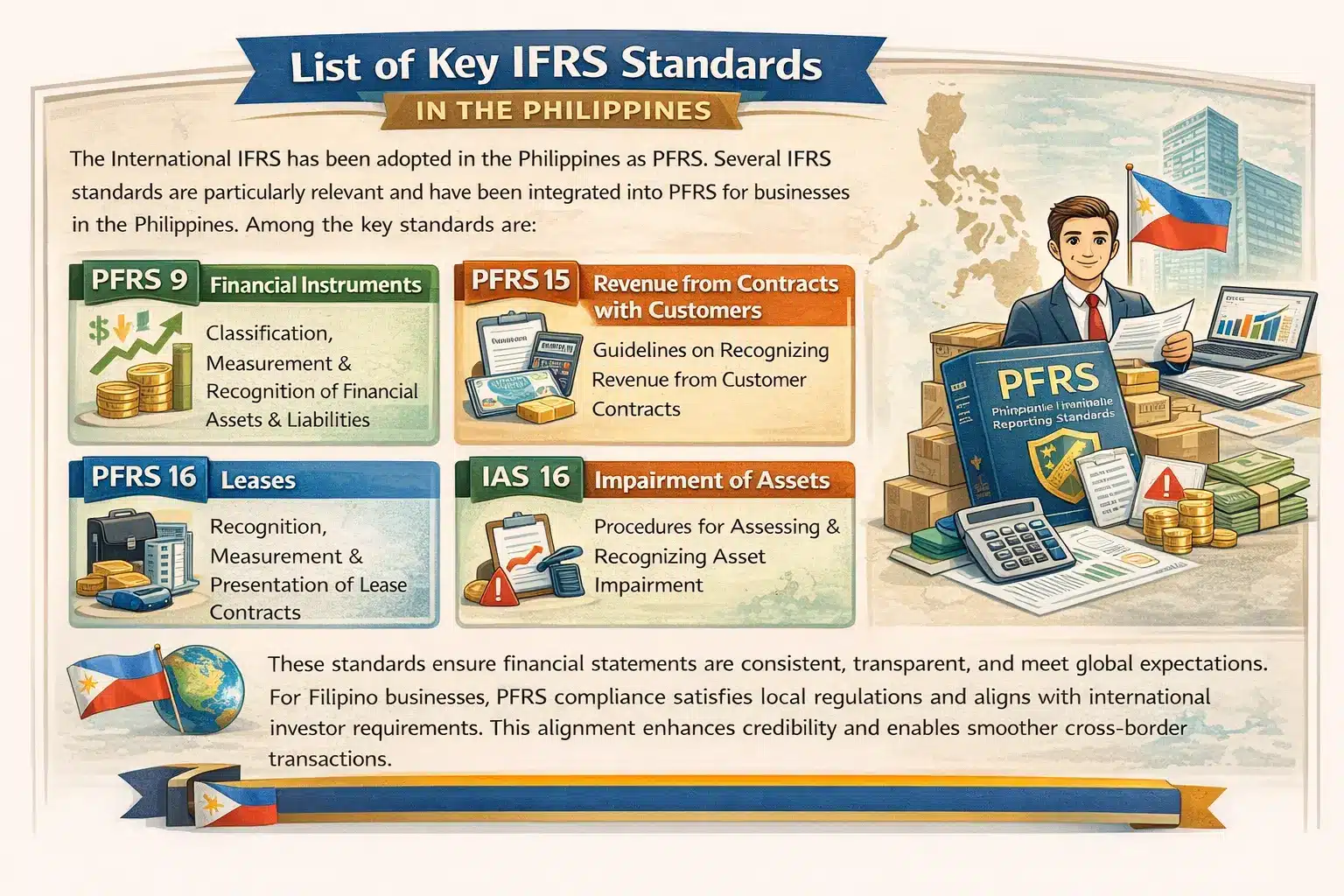

List of Key IFRS Standards

The International IFRS has been adopted in the Philippines as PFRS. Several IFRS standards are particularly relevant and have been integrated into PFRS for businesses in the Philippines. Among the key standards are:

- PFRS 9: Financial Instruments – Governs the classification, measurement, and recognition of financial assets and liabilities.

- PFRS 15: Revenue from Contracts with Customers – Provides guidelines on how and when to recognize revenue from customer contracts.

- PFRS 16: Leases – Addresses the recognition, measurement, and presentation of lease contracts.

- IAS 16: Property, Plant, and Equipment – Covers the accounting for tangible fixed assets, including acquisition, depreciation, and disposal.

- IAS 36: Impairment of Assets – Focuses on procedures for assessing and recognizing asset impairment when their value falls below recoverable amounts.

These standards ensure financial statements are consistent, transparent, and meet global expectations. For Filipino businesses, PFRS compliance satisfies local regulations and aligns with international investor requirements. This alignment enhances credibility and enables smoother cross-border transactions.

Standard IFRS Requirements

The IFRS standards cover a wide range of financial reporting requirements, but here are some of the key standard IFRS requirements that companies must follow:

1. Financial Statements

Presentation of Financial Statements (IAS 1): Companies must prepare a set of basic financial statements, which typically include:

- Statement of Financial Position (Balance Sheet): Shows assets, liabilities, and equity at a specific point in time.

- Statement of Profit or Loss (Income Statement): Reports revenues, expenses, and profits or losses over a period.

- Statement of Cash Flows: Shows inflows and outflows of cash during a period.

- Statement of Changes in Equity: Reflects changes in shareholders’ equity during a period.

- Notes to the Financial Statements: Provide additional details on the financial statements.

2. Revenue Recognition

IFRS 15: Revenue from Contracts with Customers outlines how and when to recognize revenue. It emphasizes the transfer of control of goods or services to customers as the trigger for revenue recognition.

3. Leases

IFRS 16: Leases requires lessees to recognize almost all leases on the balance sheet by recording a right-of-use asset and a lease liability. This was a shift from previous standards that allowed off-balance-sheet treatment for operating leases.

4. Financial Instruments

IFRS 9: Financial Instruments provides guidelines for classification, measurement, impairment, and hedge accounting. It requires entities to measure financial instruments based on their classification (e.g., financial assets at amortized cost, fair value, etc.) and introduces a forward-looking expected credit loss model for impairment.

5. Consolidation

IFRS 10: Consolidated Financial Statements requires companies to consolidate subsidiaries when they have control over the entity, ensuring that the parent company and its subsidiaries are reported as a single economic entity.

6. Fair Value Measurement

IFRS 13: Fair Value Measurement provides a definition of fair value and outlines a framework for measuring and disclosing fair value. It emphasizes the use of market-based measurements and provides guidelines for the valuation of financial and non-financial assets.

7. Impairment of Assets

IAS 36: Impairment of Assets requires companies to test assets for impairment when indicators suggest that the carrying value may exceed the recoverable value, necessitating a write-down of the recoverable amount.

8. Employee Benefits

IAS 19: Employee Benefits requires companies to recognize and measure obligations related to employee benefits, including pensions, post-employment benefits, and termination benefits.

9. Income Taxes

IAS 12: Income Taxes establishes the accounting for income tax and the recognition of deferred tax assets and liabilities, ensuring that taxes are properly accounted for based on the timing of temporary differences.

10. Provisions, Contingent Liabilities, and Contingent Assets

IAS 37: Provisions, Contingent Liabilities, and Contingent Assets defines how to account for provisions (e.g., legal obligations), contingent liabilities, and contingent assets based on probability and reliable measurement.

11. Disclosure Requirements

- IFRS 7: Financial Instruments: Disclosures require disclosures related to the risks associated with financial instruments, including credit risk, liquidity risk, and market risk.

- IFRS 8: Operating Segments requires companies to disclose financial information by operating segments to enhance transparency and better inform users of financial statements.

12. First-Time Adoption

IFRS 1: First-time Adoption of International Financial Reporting Standards outlines the procedures companies must follow when transitioning from national accounting standards to IFRS for the first time.

What is Philippine Financial Reporting Standards?

Philippine Financial Reporting Standards (PFRS) are the official accounting principles used in the Philippines. Issued by the Financial Reporting Standards Council (FRSC) and aligned with International Financial Reporting Standards (IFRS), PFRS ensures transparency, consistency, and reliability in financial reporting.

PFRS applies to businesses, government entities, and organizations, helping them maintain compliance with financial regulations. It covers key areas such as financial statement presentation, revenue recognition, lease accounting, and financial instruments. By following PFRS, companies provide accurate, standardized reports that aid in decision-making.

Adopting PFRS benefits businesses by improving financial transparency and reducing risks. It enhances credibility, attracts investors, and facilitates cross-border transactions. Compliance with PFRS is mandated by regulatory bodies such as the Securities and Exchange Commission (SEC) and the Bangko Sentral ng Pilipinas (BSP) for banks and financial institutions.

IFRS vs. GAAP: What’s the Difference?

The Difference Between IFRS and PFRS

Philippine Financial Reporting Standards (PFRS) are aligned with IFRS but include local transition relief to suit the Philippine financial environment. These adjustments help Filipino companies comply with global standards without excessive reporting burden.

A key difference between PFRS and IFRS is that some entities are exempt from segment reporting, simplifying compliance for smaller firms. There are also localized amendments for financial instruments and insurance industries to reflect domestic practices.

Overall, PFRS vs IFRS differences are limited, as PFRS largely mirrors international standards. This alignment enables Philippine businesses to stay globally competitive while meeting national regulatory requirements.

Who Uses IFRS?

Why is IFRS Important for Filipino Businesses?

For Filipino businesses, adopting IFRS through PFRS is crucial to avoid accounting problems that could arise from inconsistent or outdated practices. Without IFRS, financial statements may lack comparability, accuracy, and transparency, leading to issues like non-compliance, misreporting, and difficulties in securing investments.

This could also hinder international business expansion due to inconsistencies in financial reporting, making it harder to attract global investors or partners.

The Philippines enforces regulations to ensure PFRS compliance, including the Securities Regulation Code Rule 68 for large and listed entities. Additionally, the PFRS for SMEs, introduced in 2010, offers a simplified framework for small businesses, making compliance easier. These regulations help Filipino businesses remain globally competitive and facilitate cross-border transactions.

Adhering to PFRS manually can be complex, especially with fair value tracking and lease accounting. Reliable accounting software automates these processes, reducing errors and ensuring compliant reporting. Automation simplifies compliance, allowing businesses to focus on growth and making accounting software indispensable for navigating PFRS requirements.

Study Case: IFRS Adoption Strengthens Financial Reporting for a Philippine Conglomerate

A large Filipino conglomerate with diversified operations faced challenges in financial transparency and comparability, particularly when dealing with foreign partners and investors. Prior to adopting international standards, its financial reports were prepared using local practices that varied from global expectations, making cross-border financial analysis and investor evaluation difficult.

In response, the company transitioned its reporting framework to Philippine Financial Reporting Standards (PFRSs), which are closely aligned with IFRS and adopted nationwide as the required reporting basis for publicly traded entities. This shift improved the clarity, consistency, and international comparability of its financial statements, helping stakeholders from analysts to lenders make better-informed decisions based on transparent financial data.

By aligning with global standards, the conglomerate enhanced investor confidence and facilitated easier access to international capital markets. The company also strengthened internal reporting processes and reduced discrepancies between local reporting and consolidation requirements for its multinational operations. These outcomes illustrate how IFRS adoption in the Philippines creates a more competitive and reliable financial reporting landscape for large enterprises preparing for growth and global engagement.

Conclusion

Frequently Asked Questions

-

Why is IFRS important in financial accounting?

IFRS is vital in financial accounting as it ensures transparency, consistency, and comparability across global markets. By adhering to these international standards, businesses can gain investor trust, streamline cross-border transactions, and maintain credibility in global operations, enabling smoother international expansion.

-

What are the 4 financial statements of IFRS?

The four financial statements under IFRS are:

- Statement of Financial Position (Balance Sheet)

- Statement of Profit or Loss and Other Comprehensive Income

- Statement of Changes in Equity

- Statement of Cash Flows

-

What are the 4 pillars of financial reporting?

Four key IFRS principles are:

- Accrual Basis: Transactions are recorded when they occur, not when cash is received.

- Going Concern: Assumes the business will continue operating.

- Consistency: Consistent application of accounting methods.

- Fair Presentation: Financial statements must represent the company’s true financial position.

-

What are the financial reporting standards?

Financial reporting standards are guidelines and principles that govern the preparation, presentation, and disclosure of financial statements. They ensure consistency, transparency, and comparability across organizations, with common frameworks including IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles).