Many businesses keep more stock than they actually need, and that excess inventory can quietly increase costs over time. Items that sit too long take up space, tie up cash, and often go unnoticed until they start affecting operations.

Lean inventory management helps businesses reduce waste, control stock more carefully, and cut unnecessary costs. In this article, you will learn what lean inventory means and how it can help improve day-to-day inventory management.

What is Lean Inventory Management?

Lean inventory management focuses on keeping only the stock a business needs to reduce waste, cut excess costs, and free up cash and storage space. With inventory aging analysis, businesses can also spot slow-moving items earlier.

This helps companies stay efficient, avoid dead stock, and respond better to changing demand.

5 Key Principles of Lean Inventory Management

Lean inventory is based on five core principles. These principles guide businesses in creating a system that eliminates waste and maximizes value for customers. Let’s take a look at these principles and how they help businesses run more efficiently.

1. Value

Focus on what customers actually need, then remove products or processes that do not support that value.

2. Value Stream

Review the full inventory process to find unnecessary steps and reduce inefficiencies.

3. Flow

Keep products moving smoothly through each stage to avoid delays, bottlenecks, and wasted resources.

4. Pull

Order or produce stock based on actual demand instead of estimates, so excess inventory stays under control.

5. Perfection

Keep reviewing and improving the system to reduce waste and make inventory management more effective over time.

7 Types of Waste in Lean Inventory

Waste is the enemy of efficiency. Lean inventory practices aim to identify and eliminate seven types of waste that commonly occur in businesses. These are areas where companies lose time, money, and resources without realizing it. Let’s break down these types of waste.

- Overproduction

Producing more than what is needed leads to excess stock, which may never sell. This not only ties up capital but also takes up valuable storage space. - Waiting

Delays in the production process lead to wasted time. Whether it’s waiting for materials to arrive or machines to be repaired, any downtime is costly. - Excess Inventory

Holding onto more inventory than necessary results in storage costs, the risk of items becoming obsolete, and tied-up cash flow that could be used elsewhere. - Transportation

Moving products unnecessarily adds no value to the customer and can result in extra costs. Efficient inventory systems minimize the transportation of goods between locations. - Overprocessing

Doing more work than necessary, such as adding extra steps in production that don’t improve the product, leads to wasted time and effort. - Defects

Faulty products that need to be repaired or replaced are a clear form of waste. By improving quality control, businesses can avoid the costs associated with defects. - Unused Talent

Failing to fully utilize employees’ skills and talents is another form of waste. By training staff and involving them in continuous improvement processes, businesses can get the most out of their workforce.

Now that we’ve identified the common types of waste, it’s clear that lean inventory helps eliminate these inefficiencies. But what specific benefits can businesses expect?

Benefits of Lean Inventory Management

Implementing a lean inventory system comes with a wide range of benefits that help businesses save money, improve efficiency, and stay competitive. Here are some of the key advantages:

- Cost Reduction

One of the main benefits of lean inventory is the reduction in expenses. By cutting down on excess inventory and eliminating waste, businesses save money on storage, production, and materials. This allows more capital to be used for growth and other business opportunities. - Faster Fulfillment Times

With a lean inventory system, businesses can respond to customer orders more quickly. By keeping only what’s needed on hand, companies can reduce delays and ship products faster, improving customer satisfaction. - Increased Stock Turnover

Since lean stock levels are kept low, businesses can quickly sell and replenish items, ensuring that products don’t sit on shelves for too long. This not only keeps inventory fresh but also reduces the risk of items becoming outdated. - Environmentally Friendly

By minimizing waste, lean inventory practices contribute to a more eco-friendly and sustainable business model. Reducing overproduction, unnecessary transportation, and excess inventory all lead to a smaller environmental footprint.

With these benefits in mind, how can businesses implement lean inventory management effectively?

How to Implement Lean Inventory in Your Business

Bringing lean inventory management into your business doesn’t have to be difficult. Here are some actionable steps to get started.

- Build Strong Supplier Relationships

A successful inventory strategy relies on strong partnerships with suppliers. By working closely with suppliers, businesses can receive materials just in time, reducing the need to hold excess stock. This ensures that the supply chain is responsive and efficient, supporting your lean goals. - Use Inventory Management Software

Utilizing inventory management software makes implementing lean practices much easier. These tools allow you to track stock levels in real-time, automate reordering, and accurately forecast demand. Incorporating techniques such as FEFO ensures that older stock is used first, reducing waste and spoilage. This approach helps maintain just the right amount of inventory without overproducing or running out.

Once you’ve started implementing lean inventory, investing in cloud inventory software can greatly enhance your efficiency.

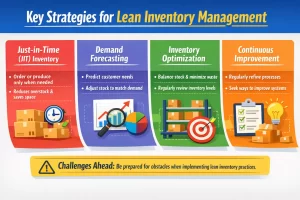

Lean Inventory Management Strategies

Here are some specific strategies that help businesses succeed with lean inventory.

Here are some specific strategies that help businesses succeed with lean inventory.

1. Just-in-Time (JIT) Inventory

This strategy involves producing or ordering goods only when needed, based on actual customer demand. JIT ensures that businesses don’t overproduce or overstock, saving money and space.

2. Demand Forecasting

Accurately predicting customer demand is crucial to maintaining lean inventory levels. By analyzing sales data and market trends, businesses can adjust their stock levels to match expected demand, avoiding overproduction.

3. Inventory Optimization

Balancing inventory levels to meet customer needs while minimizing waste is essential to lean inventory management. This requires businesses to regularly review and adjust their inventory levels, ensuring they have just enough to meet demand.

4. Continuous Improvement

Lean inventory is not a one-time fix; it requires ongoing improvement. Businesses should regularly review their processes and look for ways to optimize their systems further.

While these strategies are effective, it’s important to understand the challenges that may arise when implementing lean inventory.

Challenges of Lean Inventory Management

Like any business strategy, lean inventory management comes with its own set of challenges. However, with the right approach, these challenges can be overcome.

1. Resistance to Change

Employees may be hesitant to adopt new systems, especially if they’re used to more traditional inventory practices. Proper training and clear communication can help ease the transition to a lean system.

2. Lack of Data

It relies heavily on accurate data. Without reliable information on stock levels, sales trends, and demand, businesses may struggle to implement lean strategies effectively.

3. Technology Gaps

Outdated or inadequate technology can hinder the success of a lean system.

Conclusion

Frequently Asked Questions

-

What is inventory in lean waste?

Inventory in lean waste refers to holding more stock than necessary, which ties up capital, increases storage costs, and risks product obsolescence. It is one of the seven wastes lean management aims to reduce.

-

Why is lean inventory management important?

Lean inventory management minimizes excess stock, reduces waste, and improves efficiency. It helps businesses lower costs, respond quickly to demand changes, and streamline operations for better profitability.

-

What are the 5 rules of lean?

The 5 rules of lean are:

1. Define value from the customer’s perspective.

2. Map the value stream.

3. Ensure continuous flow.

4. Implement a pull system.

5. Pursue perfection through continuous improvement.