Are you struggling with retail accounting and finding it hard to manage your store’s inventory? Worried about how price changes might impact your profits? Have inaccurate inventory cost calculations ever caught you off guard? If so, you’re not alone.

Many business owners misunderstand retail accounting, thinking it’s all about bookkeeping. But in reality, retail accounting is an inventory management method that helps you track your stock, predict price changes, and ensure accurate cost calculations.

That’s exactly why you need retail accounting software like HashMicro’s. It automates cost tracking, gives you real-time inventory visibility, and helps protect your margins, even when prices fluctuate.

This article explores how retail accounting works, its importance, and tools to help you manage inventory, whether you’re just starting or refining your current system.

Key Takeaways

Retail accounting is a method businesses use to track and manage inventory and sales by calculating the cost of goods sold.

Accounting for retail simplifies inventory management and cost tracking, with its advantages and disadvantages, but software like HashMicro helps streamline processes and improve accuracy.

HashMicro’s accounting management software is the top digital solution in the Philippines for optimizing inventory value and cost.

What is Retail Accounting?

Retail accounting is a method used by businesses to track and manage inventory and sales by calculating the cost of goods sold. It uses the retail price of items to estimate inventory values, making it easier to manage stock levels and financial reporting.

Retail accounting software simplifies inventory management by calculating the value of stock based on retail prices. This makes it easier to handle large inventories without detailed cost tracking. This approach helps prevent stockouts during big sales and avoids excess inventory that doesn’t sell.

Getting retail software integrated with an accounting system is essential for keeping your shelves stocked with the right products at the right time, ensuring smooth and profitable operations. While it’s not traditional number-crunching, a retail management system plays a key role in maintaining a well-run store.

The Philippines Accounting Software Market underscores the need for efficient retail accounting, projected to grow at a CAGR of 6.4% from 2024 to 2030. This growth highlights the increasing demand for effective accounting solutions in the retail sector.

Advantages and Disadvantages of Retail Accounting

Accounting platforms used locally for retail can be a game-changer for inventory management. But like any tool, it has pros and cons. Knowing both helps you decide if it suits your business.

Advantages of Retail Accounting

Here are the advantages of implementing accounting for retail business:

- User-Friendly System: Retail accounting simplifies inventory management by focusing on the retail value rather than the cost price. It’s easier to track your products and manage pricing.

- Streamlined Valuation: Accounting for retail relies on consistent product pricing, making it easier to assess inventory value and prepare financial reports efficiently.

- Cost Efficiency: Accounting for retail business reduces the need for frequent manual counts, minimizing errors and lowering labor costs.

Disadvantages of Retail Accounting

Although retail accounting has many benefits, it also has drawbacks, such as:

- Less accuracy: Since retail accounting uses average markup to estimate inventory value, it might not be as precise as methods based on actual costs.

- Not ideal for all businesses: This method works best for companies with consistent markup rates. If your prices fluctuate, it might not give you the necessary accuracy.

- Potential for misleading data: If not regularly adjusted, the estimates used in retail accounting can lead to inaccurate financial reports.

While retail accounting has pros and cons, HashMicro’s software, combined with inventory management software, minimizes drawbacks and maximizes benefits by streamlining processes and enhancing accuracy.

Ready to take your business to the next level? Download the pricing scheme today and see how this aligns with accounting principles to boost your profitability. Don’t miss out on this excellent opportunity!

Differences Between Retail Accounting and Cost Accounting

Retail accounting focuses on inventory valuation using retail prices. It estimates stock value based on sales and a cost-to-retail ratio, making it useful for stores managing large inventories. This method simplifies tracking but may lack precision compared to actual inventory counts.

Cost accounting tracks production costs, including materials, labor, and overhead. It helps businesses analyze expenses, control budgets, and maximize profitability. Unlike retail accounting, which is common in stores, cost accounting is essential for manufacturers managing product costs.

Calculating the Cost of Inventory With Retail Accounting

Now that we understand what is retail account and method, let’s break it down further into two key approaches: the inventory costing method and the inventory retail method.

1. Inventory costing method

The inventory costing method is the traditional way of determining the value of your inventory based on the actual cost of goods. This method involves tracking the cost of each item from the moment it enters your inventory until it’s sold.

There are several approaches within the inventory costing method, including:

- First-In, First-Out (FIFO): This method assumes that the first items purchased (or produced) are the first to be sold. It is often used during inflationary periods because it results in lower cost of goods sold (COGS) and higher ending inventory values.

- Last-In, First-Oout (LIFO): This method assumes that the most recently purchased (or produced) items are the first to be sold. It is less common but valuable during deflationary periods or when a business wants to match current costs with revenues.

- Weighted average cost: This method calculates the cost of ending inventory and COGS based on the average cost of all units available during the period. It smooths out price fluctuations over time.

Imagine a retail store that purchases 100 units of an item for PHP 100 each and another 100 units for PHP 120 each. If the store uses the FIFO method, the first 100 units sold will be valued at PHP 100 each, while the remaining inventory will be valued at PHP 120 each.

2. Inventory retail method

The retail inventory method is more straightforward for estimating inventory value, mainly when the actual cost information isn’t readily available. This method uses a cost-to-retail ratio, which compares the total cost of the goods available for sale to their total retail price.

To calculate the ending inventory using the retail method, you can use this formula:

Ending inventory at cost = (ending inventory at retail) × (cost-to-retail ratio)

Here’s how it works:

- Determine the cost-to-retail ratio: This is calculated by dividing the cost of goods available for sale by the retail value of those goods.

- Estimate the ending inventory at retail: Subtract the total sales (at retail price) from the total goods available for purchase (at retail price).

- Calculate ending inventory at cost: Multiply the ending inventory at retail by the cost-to-retail ratio to get the estimated ending inventory at cost.

Let’s say your store has PHP 500,000 worth of goods available for sale at cost, with a retail value of PHP 1,000,000. Your cost-to-retail ratio would be:

Cost-to-retail ratio = PHP 500,000 / PHP 1,000,000 = 0.5 (or 50%)

If you have PHP 200,000 worth of goods left at retail after sales, your estimated ending inventory at cost would be:

Ending inventory at cost = PHP 200,000 × 0.5 = PHP 100,000

This means that even without knowing the exact cost of each item, you can still estimate that your ending inventory is worth PHP 100,000 at cost.

3. Bridging the two methods

While the inventory costing and retail methods have their strengths, the choice between them depends on your business’s needs. The inventory costing method offers more precision, which is crucial for companies with significant price fluctuations.

On the other hand, the inventory retail method provides a quicker, more straightforward approach, ideal for retailers prioritizing efficiency over pinpoint accuracy.

Using these methods effectively can help you manage your inventory, optimize your pricing strategy, and ultimately drive your business toward success.

Accounting for Retail Business Example

Let’s walk through an example of retail accounting. Imagine you run a clothing store and apply a 30% markup on all products. Your inventory was valued at $100,000 in the last quarter. At the end of the current quarter, you’ve generated $50,000 in sales and bought $5,000 worth of new inventory. Using retail accounting, you can determine your current inventory’s worth.

Here are the key figures in this example:

-

Beginning inventory at cost: $100,000

-

Additional inventory purchases at cost: $5,000

-

Total inventory at cost: $105,000

-

Total sales revenue: $50,000

-

Total sales with markup: $50,000 * 30% = $15,000

With these values, you can estimate the value of your inventory. To do this, subtract the total sales with markup from the total inventory at cost. This gives you $105,000 – $15,000 = $90,000, which represents your inventory value according to the retail accounting method.

Use HashMicro’s Retail Accounting Software to Optimize your Inventory Cost

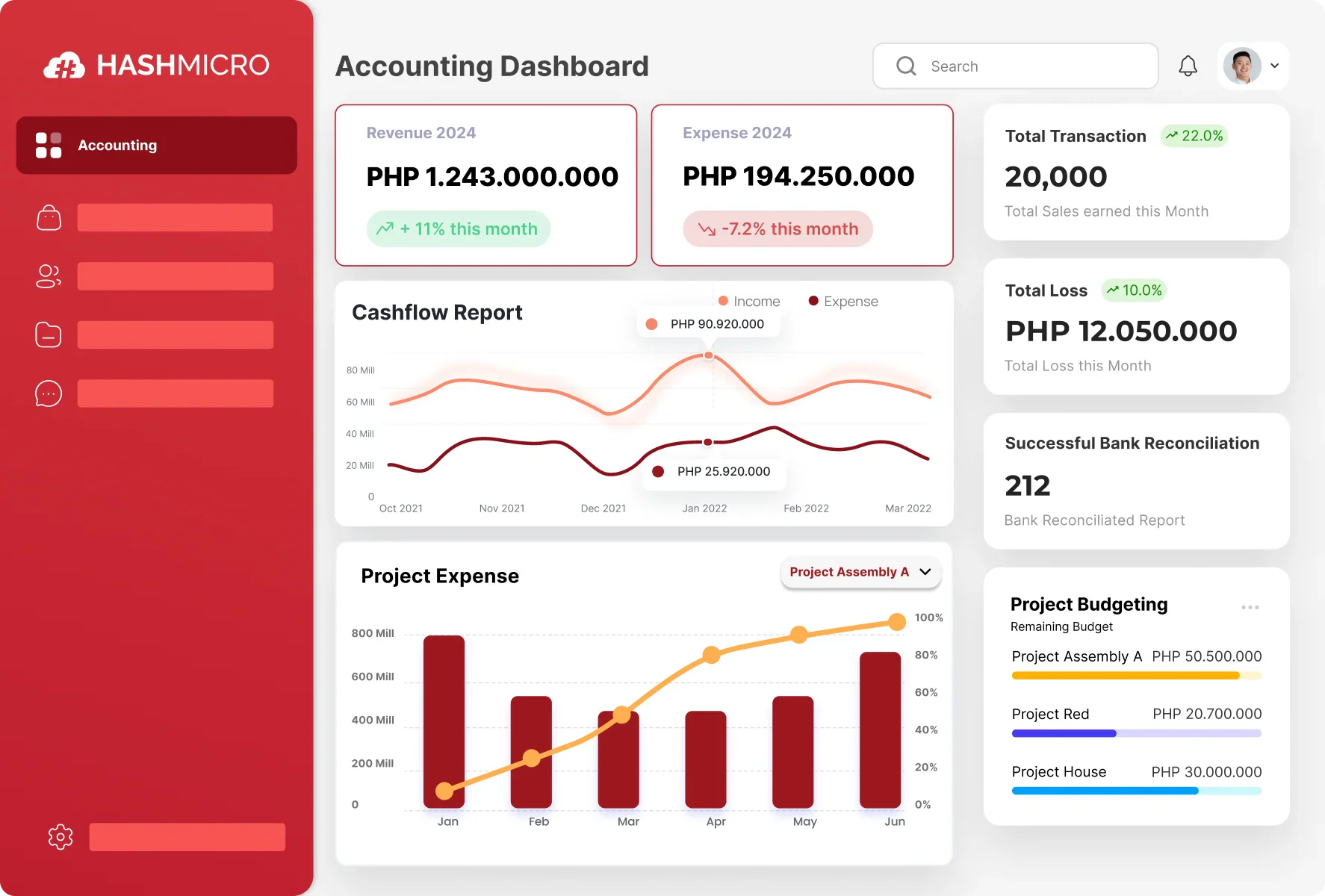

HashMicro’s retail accounting software is the top digital solution in the Philippines for optimizing inventory value and cost. It offers advanced features that streamline stock management, save time, bank reconciliation, reduce waste, and boost profitability.

You can try the AI accounting software firsthand with a free demo to explore how it optimizes inventory value and cost calculation effortlessly. It’s a golden business opportunity to experience the benefits before committing—like test-driving the future of your inventory management!

It also offers HashMicro’s inventory management software to optimize inventory cost and value by seamlessly tracking stock movements. This ensures you always know what’s in each location. Features like low stock notifications and demand forecasting help you maintain optimal stock levels.

The operational dashboard gives you real-time visibility of all stock activities, allowing you to make informed decisions quickly. Plus, by minimizing waste through better inventory turnover management, you can sell older stock first, saving costs and increasing profitability.

Features:

- Stock forecasting: This feature predicts future stock needs using historical data, helping you avoid overstocking or understocking to control costs and maintain optimal inventory levels.

- Run rate reordering rules: Automatically trigger reorders based on sales and inventory levels, ensuring you never run out of essentials while optimizing turnover and minimizing costs.

- Fast-moving, slow-moving stocks analysis: This analysis identifies fast-selling products, helping you prioritize high-demand items and cut costs on the slow-moving stock. By focusing resources effectively, you can directly boost profitability.

- Stock optimizer per warehouse: Tailors inventory management to each warehouse’s needs, optimizing stock levels for efficiency, reducing excess inventory, and cutting costs while improving operations.

- Quality control management: Ensures only high-quality products enter your inventory, reducing losses from defects or returns and maintaining consistent stock value.

These features work together to streamline inventory management, helping you keep costs down while making your business more efficient and profitable. Don’t wait until inventory issues start. Access the free demo now and see how HashMicro can transform your inventory management. It’s a small step that could lead to big profits—why not try it?

FAQ About Retail Accounting

Retail accounts track a store’s sales, purchases, expenses, and inventory. They help businesses monitor profits, manage stock levels, and ensure accurate financial reporting, making them essential for effective retail accounting.

The retail method in accounting estimates inventory value by subtracting sales from total goods available, using a cost-to-retail price ratio. It simplifies tracking but may not be as precise as actual.

Retail accounting focuses on inventory valuation using retail prices, while cost accounting tracks production costs, expenses, and profitability. Retailers use retail accounting for pricing, while manufacturers rely on cost accounting for expense control.