Managing a business means juggling many responsibilities, and at the heart of all that is working capital. It’s the cash flow lifeline that keeps your day-to-day business afloat, covering everything from supplier payments to salaries and rent.

Without the right capital, even profitable businesses can struggle with late payments, missed opportunities, and mounting stress. This includes paying for suppliers, salaries, rent, and other essential expenses that keep the business running smoothly.

In this article, we’ll break down what working capital really is, why it’s so important, and how you can manage it to keep your business stable and ready for whatever comes next.

Key Takeaways

|

Table of Contents

What is Working Capital?

Working capital, or net working capital (NWC), is the difference between a company’s current assets—like cash, accounts receivable, and inventory—and its current liabilities, such as accounts payable and short-term debts. It helps measure a company’s short-term financial health and efficiency.

A company with positive capital has more assets than liabilities, meaning it can invest in growth and expansion. But if liabilities exceed assets, resulting in negative working capital, the company may struggle to grow, pay creditors, or even avoid bankruptcy.

The amount of working capital needed depends on the industry, company size, and risk level. Businesses with long production cycles need more capital because they take longer to sell inventory. On the other hand, large retail companies that sell products quickly and receive daily payments often need less net work capital.

Importance of Working Capital

Working capital helps businesses fund daily operations and meet short-term financial commitments. With enough working capital, a company can continue paying employees, suppliers, taxes, and interest, even during cash flow difficulties.

It also supports business growth without relying on debt. If borrowing is necessary, having positive working capital improves the chances of securing loans or credit.

Finance teams focus on two key goals: monitoring available cash in real time and ensuring the company maintains enough work capital to cover liabilities while allowing room for growth and unexpected expenses.

Advantages of Working Capital

Working capital plays a crucial role in keeping a business financially stable, especially during seasonal fluctuations. Here are some key advantages:

- Balances revenue fluctuations: Helps businesses manage seasonal sales cycles by ensuring funds are available during slow months.

- Supports bulk purchasing: Allows companies to buy extra stock in advance to prepare for peak seasons.

- Ensures financial stability: Helps cover fixed expenses like rent and payroll, even during low-revenue periods.

- Aids workforce management: Enables hiring temporary staff for busy seasons while maintaining sustainable permanent staffing levels.

Limitations of Working Capital

Working capital provides valuable insights into a company’s short-term financial health, but certain limitations can make it misleading. Here are four key drawbacks:

- Constant Changes: It fluctuates frequently as most current assets and liabilities change during business operations. By the time financial reports are prepared, the company’s working capital position may already be different.

- Asset Composition: It doesn’t account for the type of assets a company holds. A business may have positive working capital, but if most of it is in accounts receivable, cash flow problems can arise if customers delay payments.

- Asset Devaluation: The value of assets can drop unexpectedly. Customer bankruptcies may affect accounts receivable, inventory may become obsolete, or theft can reduce cash reserves, all impacting the work capital.

- Hidden Liabilities: The calculation assumes all debts are accounted for, but in fast-moving businesses or mergers, missed agreements or unprocessed invoices can lead to inaccurate figures.

Components of Working Capital

Working capital includes a company’s current assets and liabilities, which are recorded on the balance sheet. However, not all businesses require every component. For instance, service companies without inventory exclude it from their working capital calculation.

Working capital includes a company’s current assets and liabilities, which are recorded on the balance sheet. However, not all businesses require every component. For instance, service companies without inventory exclude it from their working capital calculation.

So, what are the components of a net work capital? Here are the full explanation:

Current Assets

Current assets are short-term economic benefits expected within 12 months. These assets represent potential cash inflows if liquidated.

- Cash and cash equivalents: All available funds, including foreign investments and low-risk short-term holdings like money market accounts.

- Inventory: Unsold products, including raw materials, work-in-progress, and finished goods.

- Accounts receivable: Cash owed by customers for credit sales, adjusted for potential non-payments.

- Notes receivable: Cash claims documented by signed agreements.

- Prepaid expenses: Payments made in advance for future expenses, which are difficult to convert into cash but still hold short-term value.

- Other assets: Additional short-term holdings, such as deferred tax assets that reduce future liabilities.

Current Liabilities

Current liabilities are debts due within 12 months. The goal of working capital analysis is to determine if current assets can cover these obligations.

- Accounts payable: Outstanding vendor payments for supplies, utilities, rent, or other operating costs, typically due within 30 days.

- Wages payable: Unpaid employee salaries, usually covering up to one month’s worth of wages.

- Current portion of long-term debt: The part of long-term debt due in the next 12 months.

- Accrued tax payable: Taxes owed to the government, even if payment is scheduled for later in the year.

- Dividends payable: Declared but unpaid shareholder dividends, which must be fulfilled.

- Unearned revenue: Advance payments for services yet to be completed, which may need to be refunded if obligations aren’t met.

How to Calculate Working Capital

To calculate working capital, subtract a company’s current liabilities from its current assets. Public companies disclose these figures in financial statements, but private companies may not always make this information available.

Working Capital = Current Assets – Current Liabilities

The capital is usually represented as a peso amount. For instance, if a Filipino company has ₱5,000,000 in current assets and ₱2,000,000 in current liabilities, its working capital is ₱3,000,000.

This means the company has ₱3,000,000 available for short-term needs, such as covering expenses or seizing business opportunities.

A business can have either positive or negative working capital:

- Positive capital: This means the company’s current assets are greater than its current liabilities. It indicates that the business has enough short-term resources to cover its debts and may even have extra cash available after settling all liabilities.

- Negative capital: This occurs when current assets are less than current liabilities, signaling that the company may struggle to meet short-term obligations. It often points to liquidity issues and potential financial difficulties.

While negative capital isn’t always a bad sign—it depends on the business model and lifecycle—sustained negative working capital can create serious financial challenges over time.

Also, most businesses often use accounting software to automate the calculations of working capital, as there are so many components to track, group, calculate, and sort. So, if you’re interested in trying out the software to make your workflow easier, click on the banner below!

Examples of Working Capital

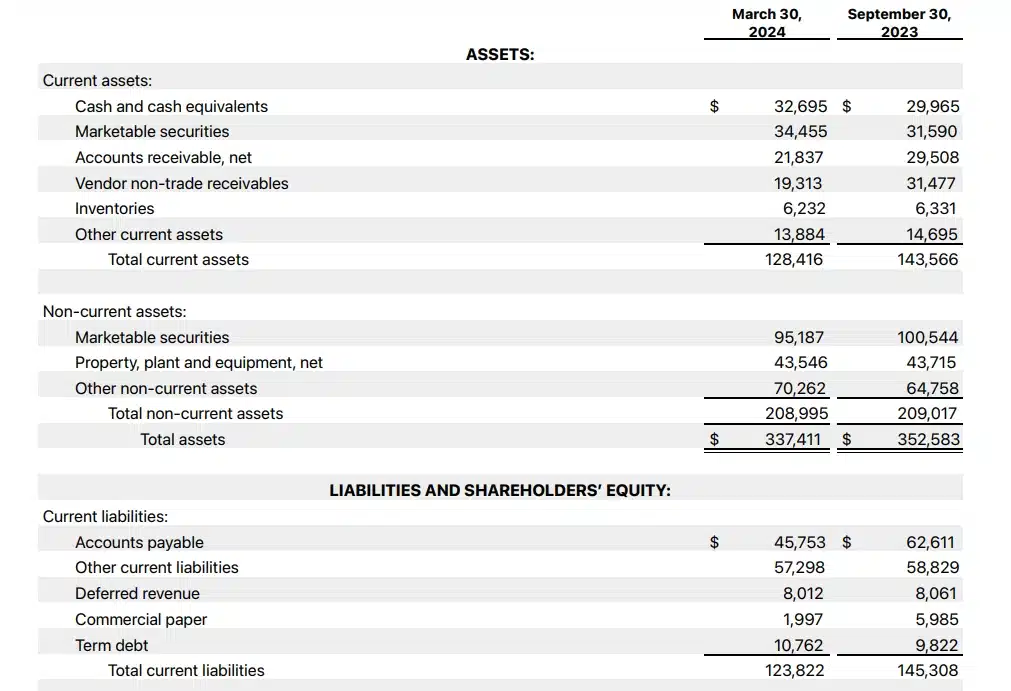

As of March 30, 2024, Apple Inc. (AAPL) reported $128.416 billion in total current assets, which included cash, cash equivalents, marketable securities, accounts receivable, inventories, and other current assets.

As of March 30, 2024, Apple Inc. (AAPL) reported $128.416 billion in total current assets, which included cash, cash equivalents, marketable securities, accounts receivable, inventories, and other current assets.

The company also reported $123.822 billion in total current liabilities, consisting of accounts payable, deferred revenue, commercial paper, the current portion of long-term debt, and other current liabilities.

Therefore, as of March 30, 2024, Apple’s working capital was approximately $4.594 billion. If Apple were to liquidate all short-term assets and settle all short-term liabilities, it would have around $4.6 billion remaining.

Special Considerations

Large projects, such as expanding production or entering new markets, often require significant upfront investment, which will temporarily reduce cash flow.

Companies that need additional capital or struggle with inefficient working capital can improve cash flow by securing better payment terms with suppliers and customers.

However, having excess working capital isn’t always ideal. It could mean the company is holding too much inventory, not investing surplus cash, or missing out on low-interest financing opportunities.

Another important metric is the current ratio, which compares current assets to current liabilities. Unlike working capital, it expresses this relationship as a percentage rather than a currency value.

6 Tips to Increase Working Capital

A business may need to increase its capital to cover project costs or handle a temporary sales decline. This can be done by raising current assets or lowering current liabilities through these methods:

- Taking on long-term debt – Borrow money for immediate cash flow without adding to short-term debt, keeping liabilities manageable.

- Refinancing short-term debt – Convert short-term loans into long-term ones to extend repayment periods and reduce immediate financial strain.

- Selling illiquid assets – Turn non-cash assets, like old equipment or unused property, into liquid funds to boost current assets.

- Cutting unnecessary expenses – Review spending and eliminate non-essential costs, lowering financial obligations.

- Optimizing inventory management – Reduce overstocking by adjusting purchasing patterns, preventing excess goods from becoming obsolete.

- Automating accounts receivable tracking – Speed up customer payments by using digital invoicing and payment reminders to improve cash flow.

Improve Your Working Capital with HashMicro’s Smart Accounting Solution

Many businesses struggle with working capital, not because they lack revenue, but because they are strapped for cash. Late payments from customers cause cash shortages at minsan, hindi napapansin ang ibang gastos habang unti-unting nauubos ang pondo.

Many businesses struggle with working capital, not because they lack revenue, but because they are strapped for cash. Late payments from customers cause cash shortages at minsan, hindi napapansin ang ibang gastos habang unti-unting nauubos ang pondo.

One of the easiest solutions is to invest in HashMicro Accounting Software, as it’s capable of tracking cash flow in real-time, documenting every transaction in detail, and thus help finance teams improve their capitals.

So, how does HashMicro help with increasing your overall financial control? Here’s how, explained:

- Direct & Indirect Cash Flow Reports – Tracks real-time cash inflows and outflows, categorizing transactions into operational, investing, and financing activities.

- Debt Collection Management + Auto Follow-Ups (Email & WhatsApp) – Records overdue receivables, sorts them by aging period, and automates payment reminders via email and WhatsApp.

- Bank Loan & Working Capital Loan Tracking – Logs loan details, including principal, interest, repayment schedules, and outstanding balances, while tracking scheduled payments.

- Online Payment / E-Invoice – Generates electronic invoices with integrated online payment options, supports multiple payment gateways, and tracks invoice statuses.

- Simple & Comprehensive Budgeting (Monthly, Carryover, Purchase Control) – Allows businesses to set and monitor monthly budgets, factor in carryover balances, and enforce purchase control settings.

Conclusion

Working capital is what keeps a business alive and maintains financial stability. When managed properly, there’s always enough cash for expenses, expansion, and avoiding financial problems. But what if you’re still manually tracking cash flow, payments, and expenses?

It’s stressful and a waste of time! So, let HashMicro Accounting Software do the work for you! It can display real-time financial data, automate invoicing and filling out reports, and know where every peso goes. No more chasing late payments or guessing games with your budget!

With HashMicro, receivables tracking is effortless, loan monitoring is easy, and working capital is optimized—no hassle! Are you ready to level up your financial control? Leave the manual work behind, and let HashMicro take care of it while you focus on growing your business.

So, try the free demo now, no commitment needed, and contact our expert team!

Frequently Asked Questions on Working Capital

-

What is the cash flow cycle?

The cash flow cycle (also called the working capital cycle) shows how long it takes a business to turn its current assets — like inventory and money owed by customers — into cash. A shorter cycle means the business gets its money faster, which helps it stay financially healthy and run smoothly.

-

How does day-to-day funding impact cash flow?

A company’s daily funding directly affects its cash flow. Good management means there’s always enough money to pay bills and invest in growth. Poor handling can lead to cash shortages, making it hard to pay suppliers, employees, or take on new opportunities.

-

Why does short-term liquidity affect a company’s value?

A company’s ability to meet short-term financial needs impacts how attractive it looks to investors. When a business has more liquid resources than short-term debts, it’s seen as stable and ready for growth — but if it struggles with cash, its value can drop.

-

What are some ways to manage short-term finances better?

Businesses can improve short-term financial management by keeping just the right amount of inventory, negotiating better payment terms with suppliers, getting customers to pay faster, and delaying their own payments without facing penalties.