Year-end accounting is a pivotal process that ensures a company’s financial health and readiness for the upcoming year. For managers, it is a time of high pressure, requiring meticulous attention to detail amidst numerous operational responsibilities.

One of the biggest hurdles in year-end accounting is the lack of accurate data and the reliance on manual processes. These issues often lead to delays, inconsistencies, and challenges in meeting audit and tax deadlines.

According to BusinessWorld Philippines, over 60% of businesses in the Philippines cite inefficiencies in financial management as a primary concern during year-end periods. This underscores the importance of adopting advanced tools to improve accuracy and save time.

This article delves into actionable tips and best practices for year-end accounting to help you navigate this critical period. Learn how HashMicro’s accounting system can transform your closing process, and take advantage of our free demo to experience the benefits firsthand.

Table of Contents

What is the Year-End Accounting?

Year-end accounting is the process of finalizing a business’s financial records at the end of a fiscal or calendar year. This essential task ensures that all account balances are accurate, discrepancies are addressed, and the business is ready to start the new reporting period with a clean slate.

The accounting year-end process involves reconciling accounts, closing temporary accounts, and preparing financial statements such as balance sheets, income statements, and cash flow statements. These steps provide a clear picture of the company’s financial health and help meet compliance requirements with applicable accounting standards.

To simplify this process, businesses often rely on a year-end accounting checklist to ensure all necessary tasks are completed. Whether following a continuous accounting method or a periodic close, year-end accounting supports accurate financial reporting and offers valuable insights for strategic decision-making in the upcoming year.

Why is The Year-End Close so Challenging?

Year-end accounting is crucial but often daunting for businesses. It requires a meticulous review of financial transactions accumulated throughout the year. This process involves collaboration across teams, including finance leaders, accountants, and employees, making it susceptible to common challenges.

Below are some of the major roadblocks encountered during the accounting year-end process, including common accounting problems such as data discrepancies and inefficient reconciliation procedures.

1. Manual errors: Manually logging transactions in spreadsheets and reconciling receipts often results in errors that are difficult to identify and correct. These mistakes can disrupt the year-end accounting checklist, delaying the preparation of accurate financial reports.

2. Disorganized workflow: When financial records are scattered across teams or stored inconsistently, consolidating data becomes challenging. Accountants may face delays in tying the books, leading to inefficiencies during the year-end accounting process.

3. Missing documentation: Employees often misplace or omit receipts and other important records from expense reports. This forces finance teams to spend valuable time chasing down missing documentation to complete the accounting year-end.

4. Compliance challenges: Staying audit-ready requires companies to prepare financial statements accurately within strict timeframes. Failure to meet compliance standards during year-end accounting can result in penalties or reputational damage.

Addressing these challenges with clear processes and modern tools can help businesses streamline their year-end accounting checklist, ensuring a smoother and more efficient close. By doing so, companies can focus on leveraging financial insights for strategic planning rather than struggling with operational bottlenecks.

Year-End Accounting Checklist

Closing your books at the end of the fiscal year is a vital process to ensure financial accuracy and compliance. A year end accounting checklist provides a clear roadmap for completing this task efficiently and avoiding last-minute challenges.

Here are ten essential steps for a successful accounting year end:

1. Prepare a financial close schedule

Creating a detailed financial close schedule ensures every task is accounted for and evenly distributed across the team. This proactive approach prevents last-minute scrambling by outlining specific reconciliation tasks and assigning responsibilities.

Finance teams should list all accounts and deadlines to keep the process on track. Planning ahead allows your team to complete the year end accounting process in an organized manner.

2. Compile all necessary documents

Gather all essential financial documents, including bank statements, tax returns, payroll reports, and sales records. Ensuring receipts and other transaction details are properly collected minimizes gaps in your records.

Using expense management software can automate this process, mapping transactions directly to your general ledger. This step lays the foundation for an accurate year end accounting checklist.

3. Review accounts payable and receivable

Examine accounts payable to verify vendor invoices, balances, and accrued expenses. Similarly, check accounts receivable to confirm customer balances, write-offs, and bad debts. Ensuring all transactions are accurately recorded prevents discrepancies in financial statements. This thorough review is crucial for maintaining financial integrity at the end of the accounting year.

4. Collect past-due invoices

Identify outstanding invoices and follow up with customers to ensure payments are received before the closing deadline. Offering payment plans or setting clear due dates can increase the likelihood of resolving past-due amounts.

Monitor accruals for unpaid revenues or expenses and ensure they are recorded in your balance sheet. This step helps maintain cash flow visibility and reduces financial uncertainties.

5. Reconcile all transactions

Compare your bank accounts, credit card statements, invoices, and receipts with your general ledger to confirm they match. Any discrepancies should be investigated and corrected promptly, as they may indicate errors or misuse of funds.

Documenting your reconciliation process ensures transparency and supports audit readiness. Proper reconciliation is the backbone of accurate year-end accounting.

6. Calculate depreciation expense

Depreciation accounts for the wear and tear of assets over time and must be accurately calculated. Using the straight-line method, subtract the salvage value from the asset’s cost and divide by its useful life.

This calculation should be recorded as a contra asset on the balance sheet and as an expense on the income statement. Including depreciation ensures your financial records reflect the true value of your assets.

7. Count and value inventory

Conduct a physical inventory count to ensure the numbers match your recorded data. Calculate the ending inventory by adding net purchases to the beginning inventory and subtracting the cost of goods sold (COGS).

Address any discrepancies between physical counts and recorded data promptly. This step is essential for accurately reporting inventory as an asset in your financial statements.

8. Assess payroll records

Review payroll records to ensure they accurately reflect employee salaries, taxes, and benefits adjustments. Verify compliance with tax forms like W-2s and 1099s and confirm that any promotions or withholdings are properly documented.

Accurate payroll records are critical for meeting tax obligations and maintaining employee trust. This step supports smooth financial operations into the next year.

9. Prepare financial documents

Prepare key financial statements, including the income statement, balance sheet, and cash flow statement. These documents summarize your company’s financial health, ensuring you’re ready for annual tax filings and audits.

Comprehensive financial reporting facilitates smarter budgeting and planning for the upcoming year. These statements are central to an effective year-end accounting checklist.

10. Create backups of important information

Securely back up all financial records to avoid data loss or breaches. Cloud-based storage ensures your data is safe and easily accessible for audits or future reference. Protecting sensitive financial information safeguards the integrity of your accounting year-end process.

By following this year-end accounting checklist, businesses can close their books accurately, stay audit-ready, and set the stage for a successful financial year ahead.

4 Benefits of a Year-End Accounting Checklist

A well-structured year-end accounting checklist is essential for ensuring a smooth and efficient closing process. By providing clear steps and organization, it offers businesses better control over their finances and greater visibility into their financial health.

Here are the key benefits of using a checklist during the accounting year-end:

1. Maintains compliance

A thorough year-end accounting checklist ensures your business complies with regulations such as Generally Accepted Accounting Principles (GAAP). By organizing your financial records and adhering to the accounting principles, you can avoid errors that might lead to penalties or audit complications.

This process prepares your company for potential audits by creating a transparent record of your finances. Compliance not only protects your business legally but also strengthens stakeholder confidence in your financial management.

2. Improves accuracy

Using a checklist for accounting year-end allows you to identify and correct bookkeeping mistakes while collecting missing documentation. Accurate records give you a clear view of your financial health, helping you balance debits and credits effectively.

It also minimizes the risk of fraudulent spending by ensuring every transaction is properly accounted for. Ultimately, accuracy lays the foundation for reliable financial reporting and informed decision-making.

3. Controls costs

Reconciling transactions during the accounting year-end helps you uncover overpayments, unnecessary expenses, and tax penalties. This gives you a better understanding of your cash flow and helps you allocate resources more effectively.

Enhanced cost control not only saves money but also boosts profitability, enabling your business to grow sustainably. With 58% of finance leaders prioritizing cost management, this becomes a key strategy for achieving long-term financial stability.

4. Enhances financial reporting

Closing your books accurately at year-end sets the stage for smarter financial planning and forecasting. A complete and up-to-date record of your finances improves your ability to budget and make informed strategic decisions.

Pairing your year-end accounting checklist with software that consolidates expenses, payroll, and vendor bills further enhances reporting capabilities. This holistic approach ensures your business is ready to face challenges and seize opportunities in the upcoming year.

Best Practices to Simplify Year-End Accounting

Achieving accurate financial balance is essential for ensuring the smooth operation of any business. Preparing precise and comprehensive year-end accounting reports is a key component of maintaining this balance.

These financial statements not only provide a detailed view of your company’s performance over a specific period but also offer valuable insights for planning future strategies.

By simplifying the process with proper tools and practices, businesses can streamline their accounting year-end procedures while ensuring accuracy and reliability in financial decision-making.

-

Eliminate manual processes

Manual processes, such as preparing invoices or reconciling transactions, often lead to time-consuming errors and inefficiencies. Automating these tasks using advanced accounting software Philippines can significantly reduce mistakes and improve productivity.

For example, e-invoicing systems store digital invoices, automatically update payment statuses, and send reminders directly to clients’ email addresses. By adopting automation, your year-end accounting checklist becomes simpler and more reliable.

-

Implement a better month-end closing process

Streamlining your month-end process lays the groundwork for a smooth year-end accounting process. Ensuring timely reconciliations, updating expense records, and reviewing accounts every month can prevent year-end bottlenecks. Additionally, using software to automate recurring tasks improves efficiency, allowing you to dedicate more time to analyzing financial data.

-

Create a year-end closing checklist

A structured year-end accounting checklist is essential to staying organized and on track throughout the closing process. This checklist should include tasks such as completing account reconciliations, updating inventory records, and reviewing financial statements.

By clearly outlining each step, businesses can avoid missing critical tasks and ensure all financial details are thoroughly addressed before the close.

-

Complete account reconciliations

Account reconciliations are vital to year-end accounting because they verify the accuracy of financial data. By comparing account balances in your ledger with external records, such as bank statements or vendor invoices, you can identify discrepancies and resolve them promptly. Regular reconciliations prevent errors from accumulating, ensuring a seamless closing process.

-

Closely review financial statements

Thoroughly reviewing your financial statements is crucial for creating an accurate picture of your company’s financial health. Pay close attention to income statements, balance sheets, and cash flow reports, as these provide essential data for planning future strategies.

An automated system can help identify errors, missing information, or anomalies in the numbers, saving time and improving accuracy.

-

Examine financial results

Once your statements are prepared, take the time to examine your company’s financial results and compare them to your initial projections. This analysis allows you to identify areas of success and opportunities for improvement in the coming year.

With a clear understanding of financial performance, your team can confidently make data-driven decisions to align with your business goals.

By following these best practices, businesses can simplify the year-end accounting process while enhancing the accuracy and reliability of financial reports. Adopting automated systems and structured workflows ensures efficiency and allows your organization to focus on strategic planning for the year ahead.

Achieve Seamless Year-End Accounting with HashMicro’s Powerful Accounting Software

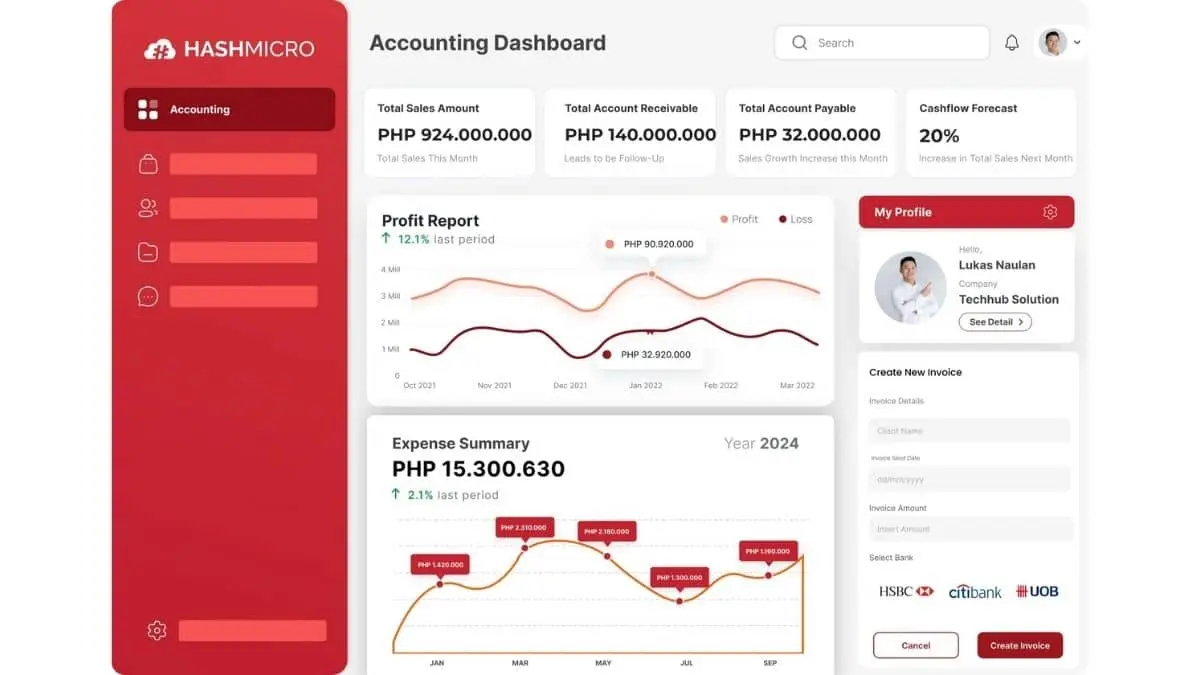

HashMicro’s Accounting Software is a powerful tool designed to transform year-end accounting into a seamless and efficient process. With automated bank reconciliations, precise financial reporting, and full compliance with the BIR’s CAS (Computerized Accounting System) requirements, it ensures businesses close their books accurately and on time.

Experience the capabilities of HashMicro’s Accounting Software through a free demo, allowing you to explore its innovative features firsthand. From real-time financial insights to automated workflows, this software is designed to enhance every aspect of year-end accounting and support smarter financial management.

Why choose HashMicro? This software automates critical processes like financial statement generation, asset depreciation, and cash flow tracking, saving time and reducing errors. Its compliance with BIR CAS standards ensures businesses meet regulatory requirements effortlessly while maintaining accuracy and efficiency in their financial operations.

Key features of HashMicro’s accounting software include:

- Bank Integrations – Auto Reconciliation: Auto reconciliation streamlines the process of matching bank transactions with your records, saving valuable time during the year-end close. It eliminates manual errors, ensuring your financial statements are accurate and audit-ready.

- Profit & Loss vs Budget & Forecast: This feature enables you to compare your actual performance against budgets and forecasts, highlighting variances that need attention. It provides valuable insights to help you plan better for the upcoming fiscal year.

- Cashflow Reports: Generate detailed cash flow reports that provide a clear picture of your liquidity throughout the year. By identifying cash inflows and outflows, you can make informed financial decisions to strengthen your year-end position.

- Financial Statement with Budget Comparison: This tool allows you to prepare financial statements that compare actual results with budgets, offering a comprehensive view of your company’s performance. It simplifies financial analysis and ensures accountability in year-end reporting.

- Complete FS with Period Comparison: Period comparison helps you analyze financial statements across different time frames, making it easier to identify trends and anomalies. It ensures that your year-end accounting is precise and aligned with past performance.

- Multi-Level Analytical (Compare FS per project, branch, etc.): With multi-level analytics, you can break down financial statements by project, branch, or department to gain specific insights. This feature ensures your year-end accounting reflects accurate, granular details for strategic planning.

- Equity Movement Report: Track equity changes throughout the year to understand how investments and earnings impact your financial position. This report provides transparency and accuracy in year-end equity management.

- Treasury & Forecast Cash Management: This feature helps manage cash flow effectively by forecasting future needs and ensuring liquidity during the year-end close. It reduces financial risks and enhances decision-making for resource allocation.

- Automated Currency Update: Automated currency updates ensure accurate reporting for international transactions, reflecting real-time exchange rates. This feature simplifies multi-currency reporting, which is crucial for global businesses at year-end.

- Chart of Accounts Hierarchy: A structured chart of accounts ensures all financial data is categorized correctly for year-end reporting. It makes it easier to generate comprehensive and error-free financial statements.

Beyond its functionality, the software offers unlimited user access, seamless third-party integrations, and customizable modules to suit your business’s unique needs. HashMicro’s Accounting Software is the ultimate solution for companies seeking to streamline year-end accounting and ensure regulatory compliance with ease.

Conclusion

Year-end accounting is a critical process that ensures your business’s financial health and compliance. However, managing this process manually can be overwhelming and prone to errors, particularly for companies handling large volumes of data.

HashMicro’s Accounting Software provides the ideal solution for businesses in the Philippines looking to simplify and optimize their year-end accounting processes. Fully compliant with CAS BIR standards, this software offers an advanced, all-in-one centralized platform that ensures accurate financial reports and effortlessly streamlines accounting tasks.

Take the next step in revolutionizing your year-end accounting by trying HashMicro’s Accounting Software today. Experience the convenience of automated processes, improved accuracy, and greater efficiency by signing up for a free demo!